WTF!?!

Now, this is a family blog, so I know that you know that acronym doesn’t stand for anything that would be inappropriate for young ears. If so, please take your mind out of the gutter. It stands for “What the fee?” in reference to mutual fund fees.

I have known for a while that the funds my employer offers through the 401k are stinkers. The funds are horrible performers, rarely beating the indices. I am a diligent saver, so I have over 200K* in my account, but I really dislike the plan. I tried to figure out how to move my money out, working up a scheme where I would quit, roll my 401k over to a decent fund family and then be rehired. My employer was less than thrilled about my idea. So, I told them what I thought of their mutual funds and trudged on.

Now, I find that I have even more reason to hate my 401k. I have often read about how mutual funds with high fees can really cut into your retirement savings, but never have given it a second thought. I know that my employer offers under-performing mutual funds, but I still never thought much about it beyond that. Regarding fees, I always thought, “big deal, what is a percent or two going to amount to?” Turns out, a whole lot, but more on that in a moment.

A couple months ago, I was reading the excellent Financial Samurai blog and noticed how Sam kept mentioning a service similar to Mint called Personal Capital. Lots of people know about Mint, but after having used Personal Capital for a while, I think it’s better. Way better. If you haven’t checked it out, its a bad-ass** tool for keeping track of your finances. Best of all, it’s free.

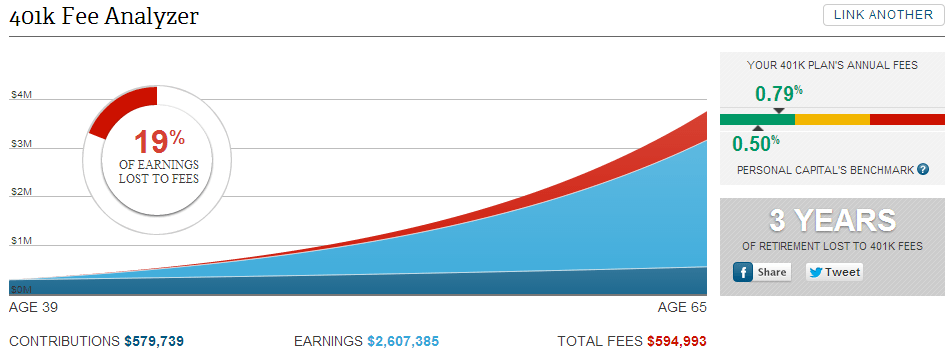

Anyway, I was playing around with one of their calculators and discovered something that blew my mind. Check out the picture below. I’ll give you a moment to pick up your jaw:

Here is the same picture, but with some commentary:

I don’t even know where to begin, so I’ll just focus on one number: $594,993. This is the amount I’ll pay in fees up until age 65. So, I’m paying some Wall Street fat cats more money in fees than most people will save for retirement to underperform the indices. ARRRRRRRGH!!! The horror, the horror!

Another thing to consider is that this graph only goes up to 65. If I live to a ripe old age of say 80, I’ll pay over $1,000,000 in fees.

This isn’t the whole truth though. The day I quit, I’ll roll my money out of this stinker of a 401k that I have now, so it won’t be nearly as bad as it seems.

However, I wonder how many people never stop to consider their funds’ fees? If you haven’t, drop what you’re doing and get over to Personal Capital. You may be surprised by what you find.

UPDATE #1!: It gets worse! Done by Forty mentioned in the comments below that some plans now charge fees above and beyond the mutual fund expenses. I looked into mine and guess what:

UPDATE #2: In the comments, James pointed me to an excellent write-up by Jim Collins regarding 401k fees. It is a must read: http://jlcollinsnh.com/2013/06/28/stocks-part-viii-b-should-you-avoid-your-companys-401k/

*You may ask why I have such a large amount in my account if the funds are bad. They were good at one point, but recently, my employer switched their provider of HR services. The funds also changed at that time.

**I’m referring to the animal. Again, this is a family blog, fit for readers of all ages.

That is heinous!!! The fees are more than your total contributions!!! Yuck.

At least you will retire soon and GET THAT MONEY OUTTA THERE 🙂

Mrs. Herb recently posted…Heath Bar Cake

Mrs. Herb, that is a really stellar (and disturbing) observation. I didn’t think about it that way. Much appreciated!

Holy Fees Bat Man!!!! I’m totally afraid to use this tool on my own 401k. The good news is that I think I can roll mine out now that I’m a 1099 worker. I’m putting that on my URGENT to-do list!!!

Great post, Mr. 1500 ~ the annotated chart was the best!

Ree Klein recently posted…Loony Logic: Student Loan Debt is Better than Credit Card Debt

Thanks Ree! Yes, do yourself a favor and take a look at Personal Capital!

Wow, that’s just crazy! It just boggles my mind how so many employers offer crap to their employees in terms of funds in the 401k plan. Why not add in some simple index funds at the very least? I really think it’s a disservice to the employee to not offer better plans. My wife’s former employer had a stinker of a plan where they only allowed quarterly rebalancing and they added a fee to do it. We talked to them countless times asking them to change but it always was just lost on them. So, we ended up doing it annually on our own. Once she left the company moving the 401k was our first call.

John S @ Frugal Rules recently posted…Paying Off Debt While Dealing With Debt Fatigue

Yes, its a total disservice! The problem is that most folks aren’t savvy enough to realize the implications.

Your wife’s 401k sounded horrible! At least I don’t have to pay a fee to shuffle my money between crappy funds.

I agree that those fees are preposterous, but luckily you (and just about anyone who retires very early) can avoid the lion’s share by simply rolling into a traditional IRA.

I recall that sometime last year employers were make available the 401k fees (like an account maintenance fee, which my employer’s plan has ($42 annually)) that are separate from the expense ratios of the funds. Not that you need to add to the horror, or anything…

Great post, I’ll go over and check out that software…maybe a change of pace is what my budget needs. 🙂

Done by Forty recently posted…We’re back, with Gratitude

Holy $#@!!! I took a look at my 401k after I read this comment and they charge me an additional $500. I am sooo mad!!!

You may be in luck. In looking at the photo you provided, it seems like that fee may be paid by your employer (“Plan”) rather than you. But your plan administrator or HR contact hopefully can confirm that.

Done by Forty recently posted…Ads, Coupons, & Savings

Yes, you are right! Thanks! Now I can back down from Defcon 4. Thanks!

I don’t worry about the fees too much. When I invest in my 401k I’m getting an immediate 100% return due to company matching. I can’t get that kind of return elsewhere. So I look at it as the fees I’ll pay over the course of my career are coming from my employers contributions. Once I retire I’ll roll over to an IRA for sure. Also, I only invest up to the company match. Above that I do my investing in dividend growth stocks in an IRA and a taxable account.

Dan Mac @ Dividend Growth Stock Investing recently posted…Philip Morris Dividend Stock Analysis

Dan, that is a great point and something that I considered putting in the post. My current strategy is to put enough money in so that I get the full match and then stop there.

Did you really ask your employer if you could quit, do a roll-over and then be rehired? That’s awesome. But you do know that your employer has a fiduciary responsibility to you, right? So if you put your concerns in writing (and preferably get other people to do the same), their fiduciary duty should kick in and force them to look into lower cost alternatives.

Our 401K fees are definitely higher than our Roth IRA fees, but we do pick the lowest fee funds, so they’re not insane. That said, I’m definitely looking forward when we leave our jobs and roll those suckers over to a nice Vanguard IRA.

Mrs. Pop @ Planting Our Pennies recently posted…Loving Where You Live

I absolutely did try. My boss thought I was nuts and didn’t even know what I was talking about at first. I explained to him how terrible the funds were and how I was happy otherwise, but didn’t want my money rotting in their account. I still don’t think he knew what I was talking about, but also had no intention of going along with my scheme. Sigh.

I work for a massive and somewhat evil corporation, so I think that my concerns would fall on deaf ears. My co-workers are fiscally irresponsible and tune out whenever I talk about finances (I am the parent on the old Peanuts cartoons: “Waaa waaa waaa waaaaa waaa…”), so I’m stuck in the mud for the moment. Thank you for the suggestion though.

My 401(k) fees are just as bad (the lowest possible fee is .8%). What we’ve done – because we have enough accounts to do it, is put all the money in my 401(k) account into that lowest possible fee option (S&P index fund), and then diversify through our other accounts. Dad’s provider offers some index funds with .05% fees! This particular strategy depends on you having other accounts that you have more control over (IRAs?, other employer 401(k)s?) and can control the fees better.

Also, check if your employer offers a “self-directed brokerage” account (or something along those lines) – you pay them a flat yearly fee (ours is $100/yr) and then you get access to all of the funds, stocks, etc at the prices/commissions that that particular brokerage charges. The savings in fund fees may easily make up that $100/year fee.

Mom @ Three is Plenty recently posted…Detailed Financial Picture – July 2013

.05%; now that is awesome!

I had the self-directed option at a past employer and asked about it this time around. I got a big, fat “No!” on that one too. I wish I had it though.

My dirty little secret is that I fiddle with the stock market and while I’ve had dumb luck, I have done really well (Google at $85 via their dutch auction IPO, Apple at $90 when the iPhone was announced January, 2007 and recently, Tesla Motors at $29 earlier this year). If I had the self directed option, most money would go to index funds and Berkshire Hathaway.

There really are some deplorable 401k plans out there. I think that in every 401k it should be required for 3 main index funds, US, bonds, and Globe-ex US. We have some index funds in my plan but they still aren’t that great on the fees, better than the active funds in the portfolio but not the best that’s available. I ran through the calculations on what I would pay in fees by purchasing individual stocks vs mutual funds and you come out way ahead with individual stocks even over some of the best index funds. Of course that’s if you have the stomach to take the higher volatility and can continue to hold and contribute when the markets head south just like with your 401k plan and have the time to devote to studying the companies. Those fees are killer and they come out whether you made or lost money. You can pretty much just tack it on to inflation for your purchasing power.

JC @ Passive-Income-Pursuit recently posted…Recent Option Transaction

Yes, index funds or self-managed would be great.

I love it when the markets tank. Look where you’d be if you dumped money into the markets in 2008. Everything is cyclical. As long as you believe the long term trend is up, buy low.

Wow, those fees really, really suck!!!

My 401K has Vanguard Institutional funds, so my fees are less than 0.10%. SO many people don’t think about the fees they get charged through their 401K. I know some coworkers pay Chase (my company’s investment partner), charges a percentage fee to manage your portfolio. That’s on top of the fees mutual funds charge. Shakes head. Don’t know how to tell them to reconsider because they think they are really smart.

SavvyFinancialLatina recently posted…Ways to Have Fun Without Dipping Into Savings

Wow, you work for a company with a sensible 401k. I just discovered I also have to pay a $500/year fee for my stupid ass plan! Grrrrrrrrrrrrrrr!!!

Caught me with the title, I was like “oh snap, something bad is going down” and indeed it was. Those are some serious fees!

KK @ Student Debt Survivor recently posted…How to Find Money for Surprise Expenses

Thank goodness for peeps like you, 1500! You keep digging and finding answers. Then you expose the villains for their treachery! Well done.

We have our $ in a target fund (2040) with Vanguard. Any thoughts on that in regard to fees?

Hope you have a feeless afternoon, 1500!

cj recently posted…Why I No Longer Eat Cheeseburgers

I’m not familiar with that particular fund, but Vanguard is typically very good about their fees.

I did have a feeless afternoon. Our little town is music crazy and tonight, they had a free concert in the big city park. Nothing like laying in the grass, looking at the sky and doing absolutely nothing (which I hardly ever get to do) for a bit.

Marvy 1500! As a guitarist, I always love to know that people are enjoying some live music, especially as they lie recumbent in the grass and let the music wash over them. Please excuse the embellishments…

cj recently posted…Why I No Longer Eat Cheeseburgers

I love the embellishments. I play guitar too and love live music. Ever been up to Austin?

Yes! Austin is marvy for everything, but music is number one. It’s classical guitar society has over 1000 members. Houston is many times larger than Austin and has only 50 or so. Shame, shame, Houston.

What do you play and what kinda music? I am a classical guy with a huge 80s metal influence. A bit of jazz in there too.

cj recently posted…Why I No Longer Eat Cheeseburgers

I am an extremely poor musician and just fart around these days. I wish I had natural ability, but I have 0, or maybe less than that.

I love classical guitar. I could listen to that all day.

I saw Buckethead last year. That guy is crazy good. If I could play 1/10 as good as him, I’d be 150x better than I am now.

CJ,

Vanguard traditionally has very very low fees. Fortunately my company also works with them to provide our 401(k)’s. I have most of my money in the Target 2050 Retirement Fund, and the fee is 0.18%

Thanks Andrew!!! Yes, 0.18%. I am glad we are not doing anything really, really, really stupid with our money.

cj recently posted…Why I No Longer Eat Cheeseburgers

Yes, do try Personal Capital! It is great, especially if you like to play around with numbers. I could mess with it all day.

That is interesting and makes a lot of sense. Most managers can’t beat the markets, so it just comes down to who is charging the least. I’ve learned a lot today; thank you!

Yes, completely frightening. I had no idea. It is painful to look at.

Holy hell! Why doesn’t every company just switch to vanguard for their 401ks? This is just waste, it doesn’t help anyone but the wallstreet firms. I like the scheme about being rehired, but it sounds a bit too complicated to be pulled off, Haha.

CashRebel recently posted…June 2013 Goals Update

Yeah, I’m on board with the Vanguard suggestion. A previous employed had a self-managed option. I loved that too. It was pretty cool being able to do whatever I wanted.

First off, love the blog and am so glad I found it! I don’t know if you follow Jim Collins but he recently did a post about 401k fees here: http://jlcollinsnh.com/2013/06/28/stocks-part-viii-b-should-you-avoid-your-companys-401k/

His general guidelines (see addendums of the post) are to absolutely contribute up to the company match. Then the tax benefits of a 401k make it beneficial to contribute as much as possible IF you plan on having a lower income during your retirement. The lower your planned retirement income the higher the benefit of a 401k.

Hi James-

Thanks for the kind comments and also for pointing me to that great post my Mr. Collins. From this year on, I am stopping at the point where I reach my company match. After that, they won’t see another cent from me.

I do hope do live on much less income in retirement though as well (no kids, no mortgage). The only expense that I see going up is health care. We shall see.

Thanks for posting the link to my piece on 401k plans, James.

Great post here, Mr. 1500. In fact I just added a link to in on my own as Addendum #5.

I love your idea of quitting, rolling and rejoining. Too bad they didn’t go along with it. But maybe this and that will help them see the light.

Vanguard…as soon as you can get it transferred.

You may have seen it already but look for “retirement gamble” on youtube. This is amazing and hearing what John Bogle had to say about fees is insane. We are getting robbed…

The Stoic recently posted…Making My Last Rental Payment; Ever?

There ARE good options (I have access to an S&P 500 Index) with an ER of 0.05%, but you have to dig and low-fee options are few and far between.

But turning on the lights should make the roaches scatter and hopefully we’ll will benefit.

No Waste recently posted…Why I’m A Boglehead (Part II)

I am convinced that HR/Company is somehow getting some sort of kickback or something through most of the investment companies. Not sure exactly how it would work, but anyway I guess I don’t have it as bad as i thought :-/ My mutual funds choices are pretty terrible, but at least they have a couple index funds that most of my money is in and have low fees (<.1%), so i can't complain about that.

Yeah, that wouldn’t surprise me at all. That or the HR people are just ignorant.

I was searching about mutual funds when I found this site. Great post here and just reminded me to check on the fees first before jumping in. I have heard this before that investing is just like shopping. 🙂

Jean @How To Make Money recently posted…Teaching Kids About Money And Financial Literacy

Hi Jean, I’m glad you enjoyed the post! I am still shocked at how much fees can set you back. http://www.brightscope.com/ is a great resource for researching this stuff.