I bought my last home in 2013. I could have paid cash for it, but instead, took out a mortgage and invested the rest. Today, I tell you how it’s worked out.

Getting Rich With A Mortgage

One of the great debates in the FIRE space is whether you should pay off your mortgage. By not paying off mine, I’m in the minority:

Most would say that they like the peace of mind that having no debt gives them and I can relate; just a little. I hate debt. Hate! Hate!! HATE it!!! I hate debt almost as much as I hate:

- Having to pee on a plane when you’re in the window seat and the guy in the middle is asleep

- Letters from the IRS

- When it’s 10 degrees outside and the kids fart in the car

- When you get done “taking care of business” and there is no toilet paper

- Humans who click pens incessantly

- Open mouth chewers

You get the picture. I DO NOT like debt. Except for the mortgage. Well, I don’t like it much either (I’d happily let you pay mine off), but I tolerate it.

Mo’ Mortgage, Mo’ Money

I bought my home in June of 2013 for $176,000. After putting 20% down, My mortgage debt came out to $140,800. It’s financed at 3.25% over 15 years. So far, we’ve paid $23,467 in interest:

Over the course of the loan, I’ll pay $37,284 in interest:

Discussing mortgage interest is boring. I know. Stick with me.

Let’s talk about the cool part; making money! Remember that I kept $140,800 by not paying cash for the home. Here’s how that money has performed in the S&P 500 with dividend reinvestment:

It’s time for some simple math:

$140,800 * .75479 = $106,274

Remember that I’ve paid $23,467 in interest to date? I’m ahead by $82,807.

If my portfolio returned $0 for the remainder of the loan, I’d still be ahead by $68,990:

$106,274 – $37,284 = $68,990

Paying cash for my home would have been a huge financial mistake!

But, that’s not the whole story. If I would have paid cash for my home, I would have been able to invest the money I’m not paying into a mortgage ($989/month) into the stock market. Let’s see how that scenario would have worked out:

Instead of having $106,274, I’d have $95,781. I’m ahead by $10,493 or about 10%. This option doesn’t beat front-loading but isn’t so bad as long as you have the discipline to invest the money instead of doing something stupid with it. Like me:

Other Things People Say

I hear excuses of why people pay their mortgage off all the time:

If I have a mortgage at 3.25%, paying it off is an automatic 3.25% return!

Even if you’re afraid of the stock market, I hope you’d keep your money in an FDIC savings account. Currently, you can get a rate of 2.25% on these accounts, so it’s a 1% return.

I just love the peace of mind that having no debt provides.

Silly human. This is an example of short-term thinking.

If you believe in VTSAX and believe in paying off your mortgage, you have a case of cognitive dissonance. Holding these two thoughts is inconsistent:

- I invest in VTSAX because it will return between 6% and 9% over the long term.

- Paying off a mortgage at 3.25% is a good idea.

Paying off a mortgage is short-term peace of mind.

A huge stack of money is long-term peace of mind.

Caveats

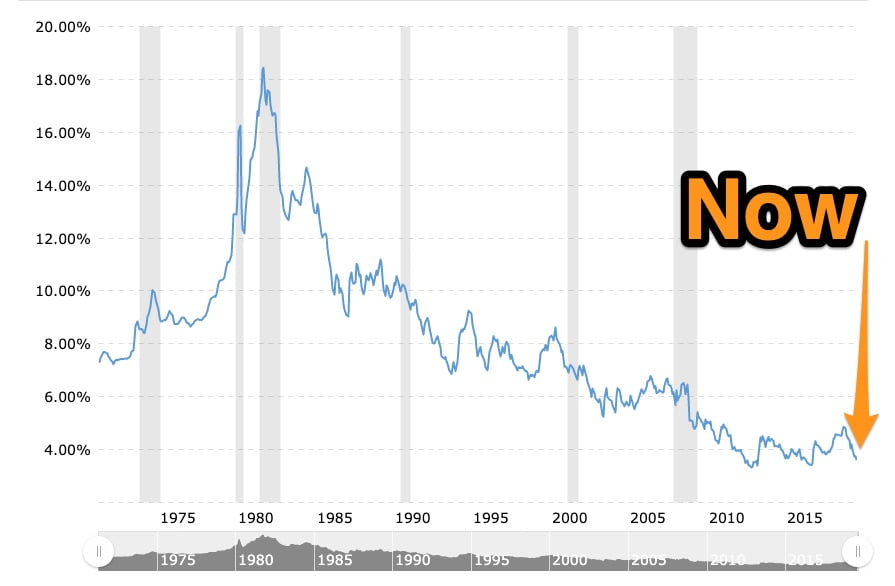

The bull has run: The stock market has been on an incredible run. I’d be surprised if the returns on the next 10 years outperform the last 10 years. However, if you have a mortgage under 4%, I’d still consider holding on to it.

Cheaper bills: If your mortgage is paid off, you can negotiate cheaper insurance because the loan holder isn’t dictating terms. Heck, if you’re OK with risk, you don’t have to have insurance at all.

Rare opportunity: Today’s rates are a historical anomaly. I’d be very surprised if they stay this way long-term.

30 Year FTW

If I could do it over again, I would have secured a 30-year loan instead. Despite my assets, I don’t have the income to refi my house to a level that would make it worthwhile (lenders are stupid and don’t care about assets).

So, I’ll just keep plugging along at 3.25%. Check back in nine years and I’ll let you know how this experiment worked out.

For another viewpoint, check out ERN’s excellent post: https://earlyretirementnow.com/2016/12/28/seven-reasons-in-defense-of-debt-and-leverage/

For an opposing viewpoint, see this guest post on Physician on FIRE: https://www.physicianonfire.com/paying-off-mortgage-mistake/

In 2015 we refi’d into a 15-year at 2.625%. We’ll pay less in interest over that entire loan than we did in the first <5 years of a 30-year 4.375% loan. Kinda feels like we're splitting the difference, which works for us; I'm willing to hedge our bets — because at the end of it, living indefinitely mortgage-free or selling and walking away with a giant check are two very reassuring options.

It also provides us with a handy target for FIRE in mid-2030. So long as the market averages at least 2.5% over the next eleven years, it's looking good!

I’m thinking about refinancing our home and pulling some money out to invest. Why not do that if you really believe in VTSAX?

We just might. We have a HELOC now that we may close in favor of a refi. The only thing holding us back is that we may be moving. We made an offer on another home on Saturday…

You made the wrong comparison. You should have compared the one-time investment in the S&P500 with a series of investments each month in the S&P. You’re a FIRE guy — you wouldn’t have just let the savings sit around or get spent!

Nope, I did that comparison too. Look towards the end of the post. This isn’t a bad option, but front-loading still wins.

I put a LOT into paying down our mortgage in the first two years instead of investing. It’s not that I don’t believe in VTSAX but when the mortgage is still over half a mil BEFORE we paid so much into principal, well… We really needed to bring down the monthly payment to something more manageable and we did so with those payments to principal and recasting twice. I’ll admit that we missed some great growth in the past two years but I accepted that trade-off in order to be reasonably sure that if the market takes a dive AND we have to sell suddenly for any reason, we wouldn’t be underwater. That was my risk aversion playing with all the trumpets and trombones. Now I’m laying off the extra payments and putting up that cash for investing instead. Who says we can’t learn? 😀

Revanche @ A Gai Shan Life recently posted…San Diego Comic Con 2019 recap

There are some great tools out there to track down loans with very loan rates and fees. I found a 10 year loan with a 2.375 rate with a local credit union. It’s hard to justify paying of a mortgage early with rates like that and no points. When searching for rates for shorter term mortgages I used bankrate.com and avoided any sites that asked for personal info, emails, or phone numbers.

The Frug recently posted…The New Frugality

First off, an Acura nsx is a sweet ride. Ignore it’s I’m practicality if u have to drive around more than you around and a lady. Second, if you pay off your mortgage early you get a “lower” rate. In your case, your rate is pretty damn low. In mine it’s at 4.65% so higher than yours. But at a 30 year. Plus we neither one are considering taxes: either on the gains and dividends nor on the tax savings of the mortgage interest. Basically it’s a whatever floats your boat situation, I think. Key is not to blow the money on stupid stuff. A NSX isn’t stupid stuff, it’s clearly a very needed transportation tool. Really, it is.

Paying off the mortgage is about reducing risks.

Many people who are investing today never experienced a major sell off in the market.

They might say they can handle it. They might say they have looked at the numbers from the past but studying history isn’t the same as experiencing it!

There is a freak show when we have 1.5% drop in the market now. Imagine what will happen when we have a simple, and routine correction?

“There is a freak show when we have 1.5% drop in the market now.”

Great point! The market will correct down 10% or maybe even 20% and it will probably do it soon (within 18 months?). People are going to FREAK out! Some members of the FIRE crowd will be caught with their pants down. There will be more recessions. Truth.

I’m in it for the long-term and so should everyone else. I fully admit this is difficult to wrap your mind around. It took me a LONG time. Hell, I hope I don’t lose my mind when it happens! 🙂

The market will correct down 10% or maybe even 20% and it will probably do it soon (within 18 months?)

Today is 25 Feb 2020 and the S&P is down 6.28% in the last two days. Could your prediction be coming true?

Get ready to start fielding calls from CNBC!

Great article Carl.

I decided in 2017 to take the market run-up and pay mine off, figuring the end of the bull had to be near. Obviously missed out on a lot of returns since then.

Curious – if you made the decision I made, would you consider taking out a mortgage now? It is strange, but the idea of taking out a loan on a paid for house to invest it “feels” like a different decision than taking out a new loan after a move, even though it really isn’t.

I would take out a mortgage now. Hell, I may be doing it in a couple of weeks when we buy a new home. That’s a little different than what you asked, but not so much.

Good post Carl.. I keep flipping between paying real estate debt off or investing the difference.

This one took me a while to come around to. I had arguments with my one of my soon-to-be FI friends here in Wisconsin about paying off the mortgage. I had been paying a little extra, in an attempt to pay off my mortgage right around the time I hit FIRE. I stopped, because frankly it doesn’t save that much. His argument that interest rates this low (mine was 3.85) are a super power people in other times won’t see. The money is better off invested – either through much better returns, or through severely discounted stock purchases that will have great value later on.

The other factor I didn’t see mentioned here, is that paying it off early doesn’t really save you 3.25%. Since the interest is amortized, you’re taking off payments at the end when you’re paying the least interest. The interest is front loaded, and anyone watching their mortgage statement can see this. In the beginning, you’re paying way more interest than principal, and that slowly flips as the payments progress.

I’m convinced. I’m just making the payments as I go now.

“His argument that interest rates this low (mine was 3.85) are a super power people in other times won’t see.”

BINGO!

Wouldn’t you feel crazy if you had paid off a mortgage of 3.85% and then in a couple of years your bank account is paying 4%? Dunno if that will happen, but it could…

Yes, I felt good writing the mortgage check today for the exact amount for the second time in a row now, knowing my investments were a little bigger because of it! Well, better slow learning than none at all haha

BC at FrugalWheels recently posted…Don’t let perfection get in the way of pretty damned good

” ..is that paying it off early doesn’t really save you 3.25%. Since the interest is amortized, you’re taking off payments at the end when you’re paying the least interest.”

You ALWAYS pay/save 3.25% (or whatever is the rate of your mortgage)! The actual interest amount will change every payment but the rate doesn’t change. The monthly interest you pay on the mortgage loan is calculated on the outstanding principal amount but with the SAME rate.

And obviously you’re taking off payments at the end by paying down your principal early. What else would you do?

I agree with Carl that paying down a low fixed rate mortgage faster isn’t the most mathematically correct thing to do, as anyone with excel and amortization knowledge should be able to figure out. Paying down the mortgage faster enables you to not have a monthly payment when you are FIRE. That’s an outgoing cashflow that won’t exist anymore (at least till you buy another house!). Some people are ok with having a monthly mortgage payment when they are FIRE. Both are ok, as long as you make that informed decision after considering all the factors.

NWA-anon recently posted…August 2019

I actually have a question for you Carl. I have a ridiculously low interest rate at 2.875% and I only have 8 years left on the loan with $112k left. However, I have thought about refinancing to a 25 or even 30 year and using the extra money per month to invest. If you had a similar situation would you refinance to a longer loan? I am trying to divorce from my head and my heart. My heart likes the idea of mortgage free, but having extra money per month to invest would be even nicer (mathematically speaking).

I would refinance, but I’d invest in real estate with at least half of the money. I’d be buying up private loans and some more exotic things like these mortgage notes that we invest in. I get a steady 10% from these, so it’s an easy no brainer.

Do you have a post about these mortgage notes you invest in? How do you find them, vet them, etc.? Do you have a 3rd party handle payment processing or is it paid directly to you and you keep track of the interest to report for taxes?

It seems like a wonderful arbitrage opportunity with potentially less volatility than the stock market, but I don’t know how to go about finding them.

Thanks!

To pay off a mortgage early, live in a home you can easily afford and pay extra each month. If you want to strategize like a millionaire and pay off your home in less than 15 years, consider Hogan’s Purchase Price Paydown method: Assume you have a mortgage of $250,000

I was pretty shocked at it only being a 10k difference if you invested each month. Maybe that 10k is worth it for the chance of stocks crashing? That would probably lessen the longer you’re holding onto it though.

3% is actually insanely high compared to the UK! We can get 1.39% with a 25% deposit over here, and we don’t have property taxes (other than stamp duty).

Not sure why the rates are so different 😮

When are you gonna write about your new house purchase? 😀

I actually botched up the calculation because it includes interest and principal. The difference is a lot more than $10,000. Stay tuned for an update.

3% is high? Whoah! Can I get a hold of one of your banks? 🙂

New home purchase! I’m going to wait until after we officially buy it. Don’t want to jump the gun. End of September…

As an American now living in the UK I can tell you there are a few differences between the US and UK markets.

1. Longer terms in the US. In the US, your age doesn’t affect your mortgage term as it does in the UK. Because of my age here in the UK, I’m only able to get a 19-year loan term.

2. UK loans are adjustable rate mortgages, usually fixed for the first 2 to 5 years, with prepayment penalties during the fixed term. The rates on a 30-year fixed term mortgage in the US is usually higher than an adjustable-rate term.

3. Higher down payments are usually required in the UK. I had to put down 15% on my new home here in the UK, and a couple of banks wanted me to put 25% down. A slight caveat, one of the banks did say the 25% down was because I was an American over here on a visa.

My loan is a 2-year fixed at 1.86% with 15% down on a 19-year term. I could have picked a shorter term but not a longer one.

In the UK, you are basically required to pay off your mortgage by the time you are around 70 to 75. I know this is starting to change and banks are offering loans up to 85+, one has gone as far as 99 years old.

While it doesn’t give you a lot of flexibility, like being able to invest in the market instead of pay off your mortgage, it does mean your living expenses are reduced by the time you are 70. That probably doesn’t mean much to the people here as most us plan on being “retired” long before we turn 70 anyways.

GrowingUpFinancially recently posted…How To Make Money By Investing In Real Estate

I have a bunch of rentals which means I have a bunch of mortgages.

A bunch of mortgages is even better than having one mortgage.

Everytime they approve me for something. I think to myself “you’re giving me how much money at 3.5%???? Who is giving me this money? Do they know how to invest?”

I feel like that Lady in the IKEA commercial 😛

https://www.youtube.com/watch?v=6C7oqXewyCE

Fire Year FIRE escape recently posted…How to make money fast with no prep work – 3 ways to maximize your pay rate

Hey Carl,

It’s been a long time! I decided a long time ago that not all decisions need to be optimized for the highest potential return. My grandfather always taught me that a bird in the hand was worth two in the bush. I’ll admit that the opportunity cost of paying off the mortgage is painful for the finance guy in me that wants to chase the highest risk-adjusted return. But my wife and I sleep really well at night knowing that our mortgage is paid off (at 32).

It’s not just the peace of mind but the mental bandwidth that is freed up when you remove the shackles of debt. It’s true that keeping your mortgage debt puts you in a position to earn potentially higher returns over the long term. But it comes at the cost of optionality.

We never paid additional principal towards the mortgage in lieu of investing, it just was a part of the overall plan. As you may recall, we set the goal to pay our mortgage off in seven years back in 2015, while simultaneously setting a goal to obtain a $10M net worth by 48. De-risking in certain areas of our life (debt), we (the royal we) had the confidence to take more risk in our careers and business opportunities.

We may have sacrificed the returns of the market on the additional $350,000 we paid toward our mortgage, but I can say without a doubt that I would have been as aggressive in other areas of my life had we not pursued the path we did. During this time I took a lot of risk in my career to make the C-Suite by age 30. Then I decided to blow it all up and start a business. We took our household income from a combined $172K in 2014 to $600K+ in 2019 (projected). Our net worth has compounded from ~$190K at December 2014 to $1.3M at July 2019.

Different strokes for different folks!

Hope you’re well.

Dom

“Different strokes for different folks!”

Haha, yeah. You’re friggin’ killing it in life, so I’m sure as hell not gonna argue with you!

Nice to hear from you again. Stay awesome and keep doing whatever the hell you’re doing!

I was completely debt here including no mortgage before moving to the UK. Since I have moved here, I did get a mortgage as I didn’t want to sell my investments to move money over from the States when the mortgage rate here was incredibly low, 1.86%.

I can say that my nerd’s brain knows it makes complete sense mathematically, the rest of me misses being debt-free.

I can say when I was completely debt-free I was able to maximize my investment strategies. I maxed out my 401K, HSA, and Roth IRA all at the same time and still have money left over to save in my taxable accounts. For me, that felt amazing. Having the extra 100K would be great especially before you hit your number, but at some point, it’s no longer about the money.

Freedom is more valuable than money. 🙂

Christopher

GrowingUpFinancially recently posted…How To Make Money By Investing In Real Estate

A 10% return is mathematically better than a 3.25% mortgage debt but math ignores risk. At your asset level the risk factor can be absorbed, so you are good with what you are doing. Most people do not have the assets to ignore the risk associated with debt. There are still people messed up from trying to do this 15 years ago. I wouldn’t recommend this strategy for people who are not in a financial position to absorb the risk.

SWFL Financial Coaching recently posted…Four Money Mistakes to Avoid

I’ve been on both sides of this debate, multiple times now. We paid off our first home, then leveraged up again once we thought the opportunity costs were too great. The leverage made us more than we otherwise would, for sure.

Then when we moved to a new place, we were sure we’d stick with that 3.75% 30 year for the duration.

Until we read Big ERN’s piece on sequence of return risk and mortgages.

https://earlyretirementnow.com/2017/10/11/the-ultimate-guide-to-safe-withdrawal-rates-part-21-mortgage-in-retirement/

I’d be interested in your thoughts on that in particular, Carl. I like the idea of leveraging up while working, but with CAPE where it is there’s no way I’d recommend someone take a mortgage into retirement right now.

Or put another way, if someone had a paid off home and they were about to retire, I certainly wouldn’t tell them to leverage up and lump sum invest the funds.

But flip that around, and people seem to like the idea of keep leverage rather than paying off the mortgage…

Done by Forty recently posted…Baby AF Goes to Europe

“Or put another way, if someone had a paid-off home and they were about to retire, I certainly wouldn’t tell them to leverage up and lump sum invest the funds.”

I would. If I could get a 30 year at under 4%, I’d get a mortgage. Even with crazy market highs, I believe that the next 30 years of the market will return more than 4% annually.

And, I’ll put the proof in the pudding soon*. We’re about to buy another home for cash (with the help of a HELOC). When we sell our current home that we have the HELOC on, we’ll own the new one debt-free. If rates are still below 4%, I’ll take out a mortgage. Stay tuned!

*With that said, the wife still works, so I fully acknowledge that mitigates some risk. If the market took a huge dump, she’d stick around for a bit longer.

I’m tots in your camp. Check out this MadFI post. I did a hybrid approach by paying down the mortgage until my payments were more P than I and then invested in a boring safe income fund. I’m now just sitting back watching the results. After a year I’m still looking good and I sleep great at night. (The bourbon helps)

A newbie here. I’ve never had a mortgage but years ago my boyfriend (now husband), decided to pay off his mortgage. At the time, it was before I started following the FIRE movement and didn’t know that much about optimization and analysis, he was hoarding cash and not investing. So, in his case, I think it made sense to just pay it off. Another thing is that we are from the Classical Music world (not the highest paying field) and income is VERY sporadic, so the mentality is to hoard cash because there is this constant feeling of insecurity about who is going book me next. Really tough out there for artist types — one of the reasons that I changed fields.

Dear Fellow Ramsey Heretic (I am sure they are issuing a fatwah against the unbelievers now), always glad to see another person go contrary to the whole “debt is evil” tribe. Another thing to consider is that a personal home, from a historical perspective is the least well performing asset you can own (thats before you deal with the horror that is selling a house). So from a balanced portfolio perspective I don’t pay extra unless my equity is less than 20% (completely arbitrary number) of my portfolio, because I really don’t want to have that much in a low performing, low liquidity (yes there are HELOC’s, but that is another hassle) asset when I can spread it out among other asset types. It helps that I have a government job and a VA loan at 3.25%….

Daniel recently posted…The 24 hour (ish) Fasting Experiment

I live in north of Europe and have an 0.32 % interest on my student loan and ca 1% interest on my apartment mortgage. Instead of paying it off as fast as I can I am putting 70% of my paycheck in a global index fund. For me it’s a no-brainer when money is basically given to you for free!

Wait one second, I read this several times and to me it looks like you made the wrong comparison…shouldn’t you compare the 106,274(gain)-23,467(interest) or $82,807 to the $95,781 meaning the paying cash option would have netted you an extra 12,974? Or you lost 12,974 by not paying cash? It is late so maybe I missed something?

Wayta go! I was wondering why you had a 15-year mortgage, until I reached the bottom of the article. My math showed that in general:

Paying off the mortgage leads to faster FIRE

Keeping the mortgage and investing the moolah leads to greater long-term wealth.

Since you reached FIRE a long time ago, you might as well keep the mortgage as long as possible! Have you tried Credible.com for refi’ing? MMM recommended it. Not sure if the loan providers they show care about income as much as others.

Mr. Bo Dangles recently posted…The Price Of Safety

I just talked to Credible actually! I think that the lenders that they deal with are traditional, so it will probably be a no-go, but I’m gonna try anyway.

1,500 Days to Freedom is another personal blog turned finance blog, written by a family man who wanted to become debt-free with a $1,000,000 portfolio within 1,500 days. In the end, he not only accomplished his goal he surpassed it.

One thing you forgot: to be in a position whether to pay $170.000 in cash or get a mortgage, you need to have the $170.000.

I’m living in Austria, I’m middle class, and don’t know many who can knock out that amount of money in cash. Especially if you don’t want to live at the arse-end of the world, when you at least need to pay double or triple that price.

Yes, systems are different here. But the only chance as a normal employee, to own a house, is to get a mortgage and pay it off slowly without putting big chunks into the stock market.

Other than that solid advice here 🙂

We did pretty well with the home purchase. It was an ugly, neglected beast that we poured a lot of time and blood into.

But yeah, $170,000 is a nice chunk of money. We worked hard for a lot of years to accumulate what he have.

How are you paying the mortgage payment? Because if you’re paying that mortgage with other income rather than your $140,800 investment, then you aren’t comparing apples to apples. You should be taking a “withdrawal” of $989.36 every month to pay your the mortgage from the $140,800 that is invested. I’d like to see what you come up with once you take a monthly withdraw from your investment, I did a quick calculation and came up with just under $60K difference, your investment would be about $150K after 74 months and subtracted your mortgage balance after 74 months (~91K). I just used your rate of return over that period of time, so in reality it could be a little lower because of fluctuations in the market and you’re withdrawing not adding to it on a monthly basis. I know it may seem like I’m arguing against your thought process, but this was the thought process I went through and decided to pay off my mortgage early and not cash it out. It’s obvious you have a higher risk tolerance than me, because there is still a chance that your investment won’t outperform your mortgage, and your initial investment will drop to zero. But the likelihood of that happening is very small, I’ve always looked at it like you have a 3.25% mortgage rate, and worse case is you are paying that interest, but there is a lot more upside potential as you pointed out. The only risk is if you don’t have a steady income, if you rely on only market returns as your income, then that’s a much higher risk, but if you have a “steady” paycheck then the risk is much lower.

I really like reading your blog and enjoy the detailed thought process behind your decisions.

Hey FI Realist! Yep, you’re correct and your “withdrawal” scenario is something I’ve thought about. Another scenario I’ve thought about is that if I have my mortgage paid off, I’ve have an extra $1,000 to put into the markets. However, I’m staying with my simple calculation for a couple of reasons:

1) It would be a huge pain in the ass to calculate this every month. I already have no time.

2) Much more importantly, front-loading usually wins and by a large margin.

One thing I am doing is keeping track of my performance. So far, I’m up $57,285 and have paid $2,975 in mortgage interest. But, we live in strange times and nothing is normal, so I don’t dare call a win yet.

Thanks for letting me know that I’ll be making a mistake if I were to pay cash for my first home. I’m not sure yet if I can commit to a long repayment plan that usually comes with home loans but reading your article also made me realize that pouring my savings into a single property purchase is not a good idea. I guess the best thing to do now is to find lending companies and compare their interest rates.

for balance… 2013 was in a raging bull market… contrast that with 2000 or 2007

The best way to look at it is to compare 30-year returns since that’s the duration of the mortgage. I googled it this morning and the worst 30 year period saw a return of 8%! Yowsers! Read more here: https://awealthofcommonsense.com/2016/05/deconstructing-30-year-stock-market-returns/