In today’s guest post, Andrew from Money Miser teaches us how to run our lives like a business.

Having a background in business and finance, I often see how the life of a business is very similar to that of a person. Day in, day out, businesses face the same kind of problems we face, yet they tend to approach them far more methodically. Businesses have a structured way of taking out the emotional aspect of decisions, while dealing with issues head on in a logical manner. They’re not emotional or selfish, they don’t splurge on self-fulfilling luxuries and they’re unrelenting in their pursuit of their goals.

Everything a business does is focused on reaching their ultimate vision, aligning with their mission and staying true to their values. Every decision a business makes is ultimately made to reach the end goal. The successful businesses are the ones that manage to do this the most effectively, and failing businesses are the ones that don’t.

I always wonder why people don’t take the same approach to our lives as businesses do to theirs. We deal with the same financial conundrums as they do, yet many of us have no process for managing them. Over at Money-Miser I’m using the foundations that many successful businesses incorporate into their strategic process for developing a structured approach to reaching financial freedom. Here’s a very succinct break-down of the strategic process.

Define Your Vision

On your path to financial freedom, you need to fully understand what your vision is. Without having an ultimate vision, you don’t have any way of creating a strategy for reaching it. How do you know how to act today if you don’t know what you want in 10 years?

Many pursuers of financial freedom do have a vision, which puts them well ahead of the majority of the population. This vision is usually something along the lines of reaching financial freedom by a given age. For us, the vision is to reach financial freedom by the age of 40, which will take over a decade.

Determine Your Values

When a business aims to pursue their vision, they determine a set of values they have to abide by along the way. Usually this is a load of PR crap like behaving with integrity, honesty and social awareness etc., but it sets the tone of how the business plans to operate.

From a financial freedom perspective it’s important to determine your values whilst you are pursuing your vision. What are your non-negotiable beliefs that you don’t want to give up no matter what your vision is? What are you unwilling to compromise on, even if it detracts from reaching your goal? This will be different for everybody, but some examples could be:

- Raising a family

- Having a pet

- Traveling the world

- Living in a specific city

- Owning a home

These are all values you place on yourself that you don’t want to compromise. Financial freedom isn’t about total and absolute frugality. We can all choose where to prioritize our spending as long as we are aware it will detract from reaching our goal along the way. The more non-negotiables you have, the longer it will take to reach your vision.

Scan Your Environment

Once a business has decided on its ultimate vision and the non-negotiable values it abides by along the way, they scan their environment. This involves developing an understanding of the internal and external environment they are operating within that will impact their success in reaching their vision.

Before you begin your journey to financial freedom, and throughout the journey, it’s important to always be aware of the environment you are operating in in order to develop a strategy around it.

Many factors need to be considered but ultimately you need to determine what your strengths, weaknesses, opportunities and threats are. Here is an example of our environmental scan:

Once you have developed an understanding of what you are doing well (strengths), where you can improve (weaknesses), opportunities you can take advantage of and threats you need to be aware of, you start to understand the big picture and you’re able to develop a strategy for reaching your vision.

Determine Your Strategy

Once a business has determined their vision, their values and assessed their environment, they can begin to develop a strategy for reaching their vision. Businesses have several different ways to pursue a strategy, some align with financial freedom and some don’t.

From a financial freedom perspective your strategy could be one of the following:

- Cost Leadership – Reduce costs to the lowest possible level to maximize savings rate

- Income Leadership – Focus is more on increasing income than reducing costs

- Differentiation – Finding unique ways to increase savings, such as moving to cheap countries, living with parents, working 3 jobs.

- Blue Ocean – All of the above at once!

Each of these strategies have their own advantages, and everybody will select a different one when pursuing financial freedom. If you have a high earning potential, an income leadership approach might be best. If you have low income potential, cost cutting might be more achievable.

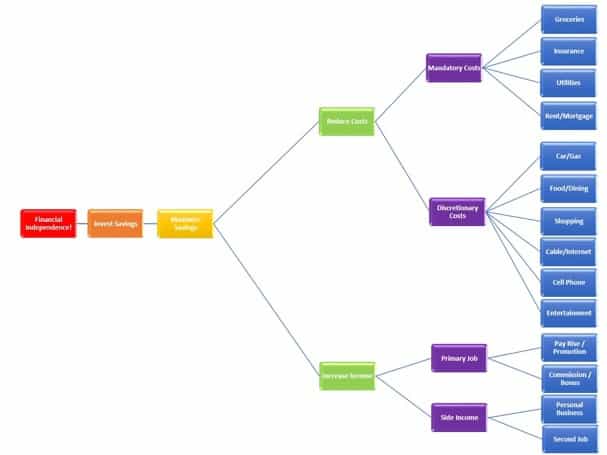

Implement The Strategy

Surprisingly, this is where most businesses and people will fail in their pursuit of any long-term goal. It’s usually quite easy to think of a vision, values and maybe a strategy, but actually implementing the strategy can be quite challenging, probably even more so for individuals than businesses. The constant temptation to spend money is unrelenting, so you need to understand how the smaller day-to-day decisions affect the overall goal.

This is where a strategy map comes in useful as it takes the ultimate vision and breaks it down into much smaller, much more manageable goals.

Using the strategy map, you can see how the smaller day to day decisions affect the much bigger, life changing goals. Many people don’t think getting rid of cable or spending less on coffee will have much of an effect on reaching their vision, when in reality it quickly adds up and the effect becomes magnified over time by compounding.

Everybody will have different ways of implementing a strategy as they all have unique visions and values. This is why blogs like 1500 Days are great resources because they provide excellent advice to help you determine your own strategy for reaching your vision. Unfortunately, no one journey is the same, so it’s not possible to give everybody equal advice.

Track Your Performance

It blows my mind how few people ever actually track their performance in life. They might set goals and vaguely work towards them without much of a strategy, but they don’t actually monitor their performance to see areas of improvement. Businesses are obsessed with this. They scrutinize their performance in an almost hedonistic manner. Every month they review their performance to see how they’re doing and where they can improve. Most people might be content with simply saving $X and the leftovers can be used however they please. This is a surefire way to be completely average.

As much as you might not like it, tracking your performance is integral for decision making and seeing where you can improve moving forward. Budgets provide you with knowledge, control, focus, short-term goals and many other advantages. Some people are opposed to budgets and tracking their spending, even MMM himself gets by without them. To this I say, be very careful. Most people aren’t MMM and as soon as they loosen their grip, their spending falls apart.

Evaluate And Respond

Businesses are constantly evaluating whether their strategy is working. Without evaluating their strategy on an ongoing basis, they’re blindly hoping that their original strategy is still effective in the current environment.

Your pursuit of financial freedom is no different. As things change in your life you need to constantly be able to respond effectively in a way that will ensure you stay on track to reaching your goal.

Strategic evaluation consists of three steps:

- Has Anything Changed? – The strategy you have chosen is based on underlying assumptions like expected earnings and expenses. These are constantly changing and the whole strategy needs evaluating whenever they do.

- Compare Actual Performance With Targeted – This is where budgeting is very useful as it allows you to see how you’re performing in numerous areas. Comparing actual results against expected allows you to see where you’re doing well and where you can improve.

- Take Corrective Action – If an assumption has changed or you find you are significantly off with your budget, you need to take corrective action. Depending on the change, this could either be a small change or an enormous change.

Obviously, if everything is going well, there is no need to make any changes; just keep doing what you’re doing!

Never-Ending Process

Managing a strategy is a never ending process of monitoring, evaluating and adjusting. Businesses never define their strategy and then ignore it, they’re always changing because something else is changing around them. If a business fails to manage its strategy it will likely get stuck in the past, fall behind and cease to exist.

You need to always stay on top of your strategy for reaching financial freedom, as soon as you rest on your laurels you’re probably falling behind. This was a very quick overview of the general strategic process. I go much more in depth over at Money Miser and will also be covering many other business topics that could help improve your journey to financial freedom, as well as less serious, lighter topics!

I’d just like to take this opportunity to thank Mr. 1500 for allowing me to guest post on his blog! I know a lot of bloggers are wary of accepting guest posts, it’s awesome he is so welcoming, even to relatively new bloggers like myself. Thanks man!

Love it. I’ve been treating my household like a business and didn’t know it for a long time.

I think tracking finances (budget and net worth) got me started but creating goals and future projections for us really put us into the business realm.

Just make sure you remember who the real Chairman of the Board is… 😉

My life is so different from how / where I thought I’d be 10 years ago, so I struggle with a specific concrete plan, A lot of what has gotten me here is flexibility of finances and attitude to go with what comes up. I’m going to keep saving and investing with FI as my goal and see where the journey takes me. 🙂

http://gph.is/22C4xWL

Ahhhhhh!!! Flashback to my old life!!!!!!

Great points all around. We tend to incorporate many of these into pout life. The most important one imho is to measure. You can’t improve what you don’t measure, and nothing is without at least some improvement opportunity.

It’s funny how it’s easier for us to ruthlessly analyze our business practices for efficiency. Why can’t we apply similar principles to our day-to-day lives? Inefficiency doesn’t happen just in the business world. 😉

Mrs. Picky Pincher recently posted…The Life-Changing Benefits of Movement

This is the real deal! Like you I have a background in business and finance, so it’s simple enough to wrap my head around an idea like this. For people who may not think this way naturally, it’s a good push to start thinking differently. There are also many folks in the community who already do think this way, but just don’t realize it yet!

Great guest post!

You’re right, the FIRE community probably inadvertently already have more of a business mind by focusing on income/spending, looking to their future and try to put plans into action today. This is what really sets the FIRE community apart from the rest, and is a large reason why they have such impressive results.

I guess you could say FIRE people are like Apple and the rest are like Blackberry haha.

Money Miser recently posted…Business Life Part VI: Strategy Evaluation

Love love love! I recently wrote a ‘how to guide’ as how I put this in practice for my own life. Absolutely incredible to see the difference when you are focusing on what matters most. I find it particularly important so that we reconnect with ‘why’ we are doing what we are doing and earning/ saving money does not ever become the actual goal but continues to be a means to an end.

Here is what Id id if anyone is interested, very similar to the concept above which I highly highly recommend (find whatever works for you!) https://traveltravelandretire.com/2017/09/13/life-development-plan-a-practical-guide-part-i/

Thank you for sharing!!!

Thank you for sharing!

PS One thing that did make me giggle – I work in HR (after many years in business and IT) where I have to do integrated analytics and planning with our finance folks, and the one thing I disagree is that values dont matter and they are BS. You literally join a company for who they are most of the time, and strong link to what they do and HOW they do it has a huge impact on engagement and satisfaction (linked to revenue).

And with that, I would just caution that solely focusing on cost cutting may prove more expensive in the long term, hence my emphasis on centering tour plan around crafting the life you WANT as a goal, and then figuring out, as part of that, how much money may be needed to align vs putting X money needed at the center of the goal with components as to why that is important to the side.

In the corporate world it happens that people are often a component vs center of a strategy, despite being 80% of our costs and literally THE single biggest competitive advantage we have. Further – aren’t we trying to do all of this to better the world for us humans? I will keep fighting the good fight despite being accused of kumbayaing the world (when to me it is in order to maximize our gains / bottom line in a sustainable way) :).

As I said, different frameworks or approaches but with the same general theory – so find one that works best for you and stick with it. Makes a big difference!

I was so excited to read this I had to comment twice. #geek. lol

Travel Travel & Retire recently posted…Personal Challenges

Haha, I wasn’t trying to say values don’t matter but it did come across like that, sorry!

I was trying to say companies like to have values to appear ethical and to act with morals. Many companies DO have great values and benefit immensely from them through attracting employees, investors and customers. However, plenty of companies like to portray good values because it makes good business sense, without actually incorporating those values into their behavior. In other words, they like to use ethics and morals as good PR rather than actually believing it. Look at the amount of companies that claim equality and equal rights yet when you actually look into their salaries you find men are paid much more. That’s just one example.

Money Miser recently posted…Business Life Part VI: Strategy Evaluation

hehe I totally get it, that is the type of work I do and discussions we have very often – made me smile bringing this into a wider conversation outside work!

Travel Travel & Retire recently posted…Monthly Challenge

my only real point was that for life, my goals are the things that bring happiness (connection, health, travel, inner peace, FIRE etc) and money is one of the means towards that goal. That is the framework I used on my link above.

Absolutely agree 100% with other comments around it being never ending process hence I think it is so important to get into the habit of thinking and analyzing if we are on track.

Travel Travel & Retire recently posted…Monthly Challenge

Having hit our FIRE number this year while also becoming empty-nesters, my partner and I are focusing on a new set of goals. What exactly do we want to accomplish for ourselves with our new freedom? We’re rounding the bend and clarifying what we want to do next.

I completely agree that “managing a strategy is a never ending process of monitoring, evaluating and adjusting.” Having financial freedom dramatically increases the range of choices and it’s important to think through them and have a way to evaluate the options and compare them to each other.

I appreciate today’s post — it’s useful and it give me some perspective.

Theres a few problems here

1. Ultimately runnning a business boils down to turning a profit, this isn’t really the same as living the socratean good-life at all, in other words, your metrics for success are completely different (if you have any morals/ethics). It sounds superficially like a good analogy to make but it isn’t really – oranges and apples

2. You don’t know now what you’ll want in 10 years – so its hard to plan for. You might think you do, but you don’t. The only way you can probably accept this is to write down what you want in 10 years time, then take a look at that in 10 years and realise you’ve changed a lot. You can only learn this through experience and its going to take you ages.

3. You have to be really clear *why* you want to be financially independent in 10 years and then realise, ideally, that all those whys you can fulfill now without having to wait 10 years if you so wish, google ‘liberate life’ for help on this angle..

4. MMM is right that tracking is good, budgets are bad. You need to know what you spend but budgets don’t work because spending is unpredictably lumpy. This becomes clear once you’ve been tracking for a few years.

I’d be wary of implementing these ideas as a ‘life strategy’, its all a bit sterile.

I would agree on the never-ending bit though, life is definitely always a ‘work-in-progress’

1. Isn’t turning a profit and increasing savings essentially the same thing? It all boils down to income and expenses at the end of the day, I don’t see any difference between a businesses financial goals and a persons. Sure, not all people care about money, but hey, this is a financial freedom blog. You can incorporate any morals and values into your plan as you wish, as stated in “determine your values” section.

2. Can’t we all agree that having more money, more time and more freedom is a good thing, for anybody? If somebody has this as their 10 year goal and they achieve it, I can’t see them looking back with regret. Find me somebody who has reached financial freedom who regrets it and I’ll be very surprised. As long as you ensure you also incorporate your values into your life, there is no reason to not have financial freedom as a goal.

3. This is possibly true, depending on what you want. That being said if your goal is to never work again and to travel the world on passive income, I don’t see how many people can achieve that now. Same can be said for raising a child without having to dump it in daycare while you work Unfortunately, life always brings you back to requiring money in some form. I don’t see how many people can fulfill these goals today unless they have a high net worth.

4. I disagree that budgets don’t work because spending is lumpy. It’s not hard to predict your lumpy spending and break it down monthly. For example, I know I have an annual car insurance in July, so I budget 1/12 of it every month. When July comes around, the money is in my bank waiting to be spent. If you have unpredictable lumpy spending, you’re not budgeting or forecasting very well. While I agree budgeting is not for everybody, it certainly works and there are plenty of people who would benefit by using one.

Money Miser recently posted…Business Life Part VI: Strategy Evaluation

I think its important to be financially savvy and in many ways thats all a business needs to be, a person needs that but much more as well though IMHO. Thats why I wouldn’t conflate the ‘ultimate vision’ of a business and a person

more money, more time and more freedom are all good things. be careful about how you trade this trinity off against each other though. I believe risk does potentially exist in trading off a decade in your twenties or thirties against later life. What I term ‘rainy-day syndrome’.

‘if your goal is to never work again and to travel the world on passive income’ this is exactly what I mean when I talk about changing goals. You may well decide that not working isn’t all its cracked up to be and you don’t really dig travelling anymore in a decade. If you want to travel the world then I would advise moving mountains to do it *now* while the itch is there to be scratched.

I’ve got quite a lot of expense tracking data, for a while I attempted to compute my own personal rate of inflation from it until i realised i was simply measuring variance, even across years. Thats why I would respectfully disagree with the veracity of budgeting on a monthly basis.

My viewpoint is that from having achieved FI already and realising theres still a whole lot more to life. There is a danger that I have observed in the FI community of using the process to defer important decisions about how to live until a later (FI) date. With the benefit of hindsight my advice would be to not make a similar error.

But that said, Your clearly smart and thinking about things, which is the critical bit. And we can all agree to disagree (I hope). But I would advise to always have a mind like a parachute, works best when its open..

I agree on most of these points – so long as it comes with the caveat that it doesn’t mean every decision needs to be purely financial, despite that being the case for a business in many cases. 🙂

More I see this as a framework for decision-making and execution of those decisions, following what many organizations do. For that purpose I think it makes a lot of sense, and it’s one I directly or indirectly employ in every decision I need to make in my personal life.

Dave @ Married with Money recently posted…Why You Should Talk About Your Finances on The First Date

Great article. I see so many people who directly jump to strategy and implementation without focussing on the 3 earlier steps that you mentioned. It’s important to know what place the business will have in our lives and how it fits with our goal (what you’ve called as Determine Your Values).

Sumit recently posted…Using FILTER Function in Google Sheets (explained with Examples)

Life is the quintessential startup—allocate your time as you would a budget, surround yourself with positive influences, and eliminate what depletes your energy. What are the gains? Fulfillment and achievement. What about the setbacks? Valuable insights gained. Approach life with leadership, and observe it flourish! 🚀💡 #LifeAsABusiness