I have a problem and it is Facebook. No, I don’t check it 500 times per day. The problem is that the stock is eating my portfolio:

On The Hook With Facebook

In May of 2012, I bought 1,000 shares of Facebook when it went public at about $41. And then it dropped, so I bought more. And then it continued to drop, so I continued to add to my position. When the dust had settled, I had bought another 1,000 shares and brought my cost basis down to about $30.

My hypothesis was simple; I thought that Facebook would smoothly move to mobile (it was a desktop experience in 2012) and that the service would be successfully monetized. Both happened and the stock now sits at around $190. I’ve since sold 550 shares, but still hold 1450 or about $275,000.

Facebook is, by far the largest investment I own. And it terrifies me. Facebook is a social network and at some point, users will get bored and move on to something else. I don’t want to be caught holding the Facebag. However, big tax bills also terrify me. But, I figured out a way out of it.

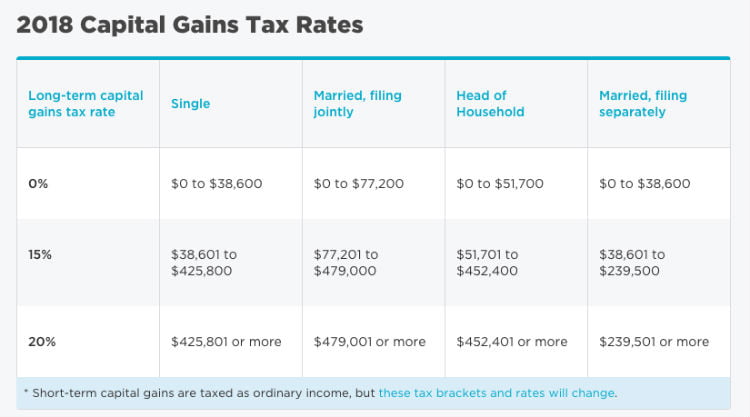

How To Pay Zero Capital Gains

For the early retiree, long-term capital gains may not be an issue. This is because you pay $0 in federal taxes if your taxable income plus your capital gains are under a certain threshold. For a married couple, it’s $77,200 and for a single person, it’s $38,600:

So, let’s say you’re married, earn $50,000/year and have $20,000 in long-term capital gains; you pay $0 in taxes for the stock sale.

#winning

However, my personal situation is a little different. Mrs. 1500 has her dream job and occasionally this blog spits out little chunks of money. While our income is variable, I think that we’ll earn more than $77,200 this year. At first glance, it looks like we’re liable for long-term capital gains. Upon deeper investigation, I found a way to avoid Mr. Taxman for most of my gains.

Standard Deduction Seduction!

To start, let’s assume that Mrs. 1500 and I make $90,000 this year. The new tax law gives us a standard deduction of $24,000, reducing our taxable income to $66,000. We’re now $11,200 below the capital gains threshold:

$77,200 – $66,000 = $11,200

I’m currently sitting on $232,000 in capital gains, so $11,200 doesn’t amount to much. At that rate, assuming all variables stay the same, it would take 20 years to sell all of it.

Standard deductions are seductive and sexy, but not overwhelmingly so. Kinda like your favorite supermodel when you were a teenager, but now you’re 35 and they’re 45. They still look good, but it will never be the same.

Hold on, the numbers get better! (However, the post doesn’t. It’s all downhill from here.)

401(k) To The Rescue!

I love 401(k)s almost as much as I love my wife, children and plastic dinosaurs.

I said “almost!” Mrs. 1500, please know that by “almost,” I mean that I love you at least twice as much as my 401(k). And I definitely love you more than I love the dinosaurs. Seriously.

Ummmmmmmmmmm…

Anyway, Mrs. 1500 has a 401(k) at her job and I have a self-directed 401(k) for my corporation. The 2018 limit for 401(k) contributions is $18,500 per person. Remember that this money comes out pre-tax. In other (and beautiful) words, it reduces taxable income. If Mrs. 1500 and I both max out 401(k)s, we’ve reduced taxable income by another $37,000. So, let’s add this to the calculation:

$90,000 (income) – $24,000 (standard deduction) – $37,000 (401(k)) = $29,000 (!!!)

We’ve reduced our taxable income from $90,000 all the way down to $29,000. Let’s revisit the capital gains calculation again:

$77,200 (upper 0% limit) – $29,000 (our taxable income) = $48,200

We can now take $48,200 in long-term capital gains and pay $0 in federal taxes. Amazing, right? Super-sexy even!

But it gets even better.

Upping The Cost Basis!

Let’s say you have a stock called Dinosaurs ‘R Us (ticker: $DRU) that’s appreciated a ton, but you want to hold on to it. If you can perform the hack described above to keep federal capital gains at $0, it may be worth selling $DRU and immediately repurchasing it. Why? It raises your cost basis, minimizing capital gains down the road.

Amazing!

This strategy is useful if you anticipate increasing income in future years. This is a real possibility for those of us who have fat 401(k) balances. For a detailed explanation of the strategy, see Michael Kitces’ excellent piece on Capital Gains Harvesting.

The Caveats

So, there is one big and one small caveat to this hackery:

The big one is state income tax. For example, my home state of Colorado charges taxes on long-term capital gains regardless of taxable income. It is low (< 5%), but it’s still there.

The other caveat is that you may just be deferring a tax bill. 401(k) withdrawals are taxed as ordinary income. Again, if you have loads of money in a 401(k), you could be hit with a required minimum distribution later in life.

Check your own state laws and your accountant to be sure of this hackery before you attempt it. I’m just a weirdo on the internet who plays with plastic dinosaurs. What could possibly go wrong?

I’m Totally Doing This (and Maybe A Tattoo Too)

While I will have to pay state income tax, I’m taking advantage of this hack to start unloading my Facebook. Mrs. 1500 and I are maxing out our 401(k)s so we can maximize the selling. I didn’t need another reason to love 401(k)s, but now I have one.

Mrs. 1500 keeps asking me if I’ll get a tattoo (she has several) (none of my likeness) (none of the dinosaurs either). I’ve always said:

NO!

But now, I’m reconsidering. I’m sure that Mrs. 1500 wants me to get a tattoo that reflects our relationship and our children, so she may be dismayed when I show up with this one instead:

Very nicely played with a great combo of the new standard deduction, 401k, and LTCG rates. One thing I would add that could help the 1500’s in your case, on a Federal level, would be the revised Child Tax Credit, which only furthers the amount of capital gains that could be recognized 🙂

Whoah, and I have kids too! Silly me for not thinking about this! Danny, I owe you the next pizza!

Amazing gains there on your Facebook stock (600%!!). I would do the exact same thing, it seems like a no-brainer. I think I love 401(k)’s as much as you do. Not only can it decrease your taxable income itself AND give you capital gains harvesting space, it can also INcreasing credits, such as for the ACA.

Yeah, I’m blown away by the power of the 401(k). All of the benefits are absolutely incredible. It’s hard to believe that something that allows you to put money away pre-tax also allows you to avoid post-tax gains. Life is good.

Great write-up as usual! Question – Don’t dividends play a factor in all this however? I imagine they’d be at least $10-15K a year of payouts for you into taxable accounts. Any tips on estimating/planning for annual dividend payouts? Having only been investing heavily in a taxable account for a few years, and making sizable contributions each year, I’m yet to get the hang of estimating it.

Yep, dividends do play a factor. In my post-tax portfolio, almost everything is in growth stocks, so I don’t have more than $1,000 in dividends per year. If I were a dividend investor, I’d try to keep those stocks to a pre-tax account. If you have a corporation, a self-directed solo-401(k) is one way to do this.

I do have investments that pay have frequent payouts (mostly syndication deals and private loans), but I keep them in that self-directed solo 401(k) so that I don’t have to worry about taxes.

“Any tips on estimating/planning for annual dividend payouts?”

I’m sorry, but this isn’t my specialty. Maybe a dividend guy will chime in?

Yea – even with just $100K in VTSAX in a taxable account, it’s throwing off $2K a year, and will only grow over the years in the future.

Self-directed Solo 401K is something like 20% of profits up to that $53K number can be contributed, right?

So, with a solo 401(k), you can put your own $18,500 in. Then, your corporation can do a 25% match on your wages. And yeah, the max is right around $53,000.

Yes! This is a perfect post explaining it. I have to admit, I’ve thought of moving to another state in retirement due to state become tax. NYC is something like 10%. Grumble grumble.

Of the 7 states, high up on my list are Texas and Florida. Though Florida is probably better, I’m slightly worried about the schools. Also, I love BBQ and the Chinatown in Houston is awesome. Plus the airport is better situated. Hmm.

10% And the winters! Yeah, go south! I think Washington is also tax-free, right?

Yep, Washington has no state tax.

Mr. Tako recently posted…The High Cost Of Eyesight

I think you also missed your business income is reduced twenty percent before your individual taxes as well thanks to the pass through provision in the law.

Those are some good strategies to lower taxable Mr. 1500. Another option might be to shove income into a HSA (which can then be invested). If you *know* you’re going to have significant healthcare costs in the future (and who won’t?).

The contribution limit for 2018 is $6900.

Mr. Tako recently posted…The High Cost Of Eyesight

Haha that tattoo would be amazing. I was reading about how this latest market run is creating 401(k) millionaires left and right. You might not be the only one to get that tattoo.

I love any post that shows how to save on taxes, compares his wife to a plastic dinosaur or uses #winning!

I really loved this one.

Jason@WinningPersonalFinance recently posted…Pay Off Debt or Invest Interview 1 (Winning Personal Finance)

Thanks for the kind comments Jason!

Great gains and tax strategy. I admire your courage, I think, but I just won’t buy individual stocks. Too much stress and not nearly enough diversity for Mr. Cautious here. My dad bought $1000 worth of WalMart stock decades ago that was worth $80,000 when my brother and I inherited it. It got a stepped up basis and so there was no tax when I sold it. It was actually in the form of paper certificates in a lock box if you can believe that, they were pretty cool. He went to one of the annual meetings once and got to ask Sam Walton a question from the audience.

Steveark recently posted…If I had a million dollars

Note that I have no interest in owning stocks anymore. I may be courageous, but foolish is another word to describe it!

That is a great story about the paper certificates. I don’t think that I’ve ever seen one!

Wait, taxable account sales/withdrawals don’t count towards ordinary income, there’s just the cap-gains tax. So my understanding is that you could sell *all* your FB for zero cap-gains if your taxable income stays under $77,200. Am I off-base here?

Yeah, it doesn’t work quite like that. I asked about it in the Choose FI Facebook group (a great resource by the way) and a finance whiz explained the IRS worksheet:

Line 1 of the worksheet says enter amount from 1040 line 43.

Line 43 is taxable income. Taxable income is AGI less standard/itemized deduction. AGI is total income less above the line deductions. Total income includes capital gains or losses (see line 13).

LTCG is definitely included in income, which means it’s included in AGI, and subsequently taxable income.

You follow this worksheet through, and you subtract 75,300 from taxable income (that’s the 2016 threshold). That gets you an amount in line 11, which is taxed at 0%.

Then, you take the remainder, and so long as that number is under 466,950 for MFJ, you tax that remainder at 15%. You can see that in line 20.

So we observe two things

1) Your LTCG does get added to taxable income, which determines your eligibility for the 0% LTCG taxes

2) All your LTCG that are above the 0% LTCG threshold are taxed at 15% (and if you have enough income, some of that is actually taxed at 20%)

Wow, thanks for clarifying that. I followed the worksheet and see what you mean. I’ve been making the wrong assumption for years and now I have to go fix my future drawdown spreadsheet!

So if you make 90 – 37 that means you actually expense live on 53K for the year ?

And you have your mortgage still ? I just can’t swing it with kids. Maybe when they are out, or home is paid off I could but, but not now. It’s a great plan if you can adjust expenses down that far. I’m just not there yet.

Yep. Our mortgage (with taxes and insurance) is $1,200/month and then we spend around $2,000 after that, so we get by on about $40,000. I’m fortunate in that the wife gets health insurance at her job. If she didn’t, a Liberty HealthShare plan would cost $449/month.

We have paid off cars, kids go to public schools and recurring expenses are minimal, so we get by with a minimal amount of money.

#firstworldproblems

Nicely done!

Financial Velociraptor recently posted…Write Puts Target (TGT)

Yep! Life is good. Screw it, life is f***ing awesome..

This is one of those ‘nice problems to have’ isn’t it?

Yep. I’m very fortunate to have it!

Couldn’t you avoid the deferred taxes on your 401k by doing a Roth conversion ladder?

Yep. I may do that as well at some point. “Lots of moving parts there are.” -Yoda

Great post. You have a real talent for simplifying our tax code. I had the same problem last year with AAPL and used a combination of a SE401K, HSA and a 529 to get my AGI and state capital gains taxes under the limit. Sort of like landing a small airplane on a runway in a crosswind.

“Sort of like landing a small airplane on a runway in a crosswind.”

Haha, yeah! While there is certainly some thought that goes into it, I think it’s kinda fun and rewarding too.

If you’re paying taxes, it means you’re making money.

Money Beagle recently posted…The Power Of Bad Habits

I like to use the system for maximum efficiency, but I’m not one of those crazy (“DON’T RAISE MY TAXES!!!!”) people either. In the last referendum, I voted in favor of every tax increase on the ballot including funding schools and building a high-capacity reservoir for our arid town. In the US, we pay some of the lowest taxes out of any first world country. I’m just fine with paying them as long as they’re being put to use efficiently.

Mr. 1500 Days,

Just found your blog. Now that’s what I call a high class problem! You did something right with this problem, btw, you didn’t “sell you winners,” which a lot of people actually do–esp stocks that double or more. I’m also impressed you held on during those first couple of months. FB is a borderline monopoly at this point; so you should be good. (I own a fair amount of tech, but not FB btw.)

I live in CO as well, and I beat you! I bailed at 42–or are you secretly going to get there by then? JK. It is very important to have a nice financial buffer before “retiring.”

Looking forward to reading more. I like your writing. Cheers!

I’m done with work, but I didn’t bail until 43. Still beats 63! Let me know next time you make it up to Boulder County!

Will look you up for sure. And ditto if you make it to southwest Denver. Cheers!

PS: I should add that I have a slightly different strategy than what you outline on this post. I’m kind of “global nomad”–ish. So I will likely have WA state as a home base at some point soon. Am delaying the cap gains strategy you outline above until I don’t have to pay state income taxes.

Also, one other real negative kicker with this strategy is if you truly go for “retirement” you may end up using Obamacare. Maximizing Obamacare benefits gets thrown out the window in a hurry if you start locking in cap gains. Why? Because the cap gains still count towards your income for Obamacare purposes even if you don’t pay any taxes on them at the federal or state level. It potentially torpedoes this approach.

Dah, another moving part that I had not considered! Thank you for that!

You bet. I was really bummed when it dawned on me that this killed my plans to step up the cost basis on a bunch of tech stocks.

Thanks for sharing this article with us,Found it very useful ,since i have very little knowledge regarding finance.

This helped me in getting through the hurdle.