Prosper.com and LendingClub.com are two websites that facilitate peer to peer (P2P) lending. What is P2P lending you ask? Wikipedia.org defines it as follows:

Peer-to-peer lending (also known as person-to-person lending, peer-to-peer investing, and social lending; abbreviated frequently as P2P lending) is the practice of lending money to previously unrelated individuals or “peers” without the intermediation of traditional financial institutions (banks). It takes place on online lending platforms that are provided by peer-to-peer lending companies on their websites and is facilitated by credit checking tools of varying complexity.

So basically, its giving uncollateralized loans to strangers over the Internet. Wait, before you run off screaming in horror and questioning my sanity, allow me to explain a bit more. Let’s start off with an example:

Sarah has $8,000 in credit card debt at 23% interest. She would like to be able to pay it off at a more reasonable rate, however loans like this are difficult to secure from a conventional bank. She learns that she can apply for a loan like this at LendingClub.com.

Similar to applying for a credit card, Lending Club runs Sarah’s credit and verifies her information. Based on her credit history, Lending Club offers her a 3 year loan at 12%. She accepts these terms and the loan gets listed on Lending Club for lenders to invest in.

Larry the lender see Sarah’s listing and likes what he sees. He decides to help fund Sarah’s loan. He can contribute any amount from $25 on up. Being a smart lender, Larry likes to be diversified, so he agrees to give Sarah $25. When other lenders have committed enough money to cover Sarah’s request of $8,000, the funds are released to her.

Every month, Sarah makes a payment and Larry gets paid. Lending Club takes care of all of that. If Sarah turns out to be a bad borrower and stop paying, she’ll have collection agencies on her tail and her credit will take a hit, again just like a credit card.

I think P2P lending is great, but when I tell people about it, they tend to think I’m crazy. “You lend money to strangers?!?!” is always the response. I sure do. You know who else does? Citibank, Discover Card and American Express. Want to see what kind of money those guys haul in?

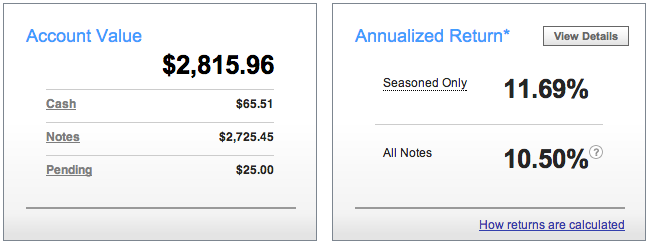

I’ve been lending on the Prosper platform since October of 2010 and on Lending Club since April of 2011. I’m pretty conservative, so I ramped up slowly, but I very much like the results. Here is a quick look at my returns:

Some things to keep in mind should you decide to jump into P2P lending:

- There is a lot to learn. Take a while to study the resources I posted below and start slowly. Get to know your way around the platforms.

- Diversify! Spread your money out. I would recommend not having more than 1 or 2 percent of your money in any one loan.

- Prosper and Lending Club are both SEC regulated. When the platforms first appeared, they were a bit rough around the edges and a lot of bad borrowers slipped through the cracks. With SEC oversight, the platforms have quickly matured.

- I started out very risk averse, only investing in the safest of loans. However, lenders with the highest returns invest in the riskier loan classes. They have greater defaults, but the higher returns more than make up for it.

- You will have defaults and some of them will be painful. There are still scammers who will make 1 or 2 payments and then are never heard from again. However, this is becoming less of an issue. Don’t dwell on defaults.

Want to learn more? Check out these sites:

- The definitive site for information is Peter Renton’s excellent Lend Academy. I highly suggest you devote a good chunk of time reviewing this site. There is a wealth of information here.

- Nickel Steamroller has an awesome portfolio analyzer (Lending Club only) and a lot of other great stuff.

- Prosper Stats is a nice tool for analyzing data from Prosper.

I truly like P2P lending more every day. I don’t think I’ll ever beat the returns of a really good year in the market, but there is a good chance I can beat the my stock portfolio over the long haul. As I get closer to retirement, I need to change my portfolio from growth to income. I see P2P lending as providing me a substantial source of this income and look forward to increasing my investments substantially.

I have much more to say on the topic. In a couple weeks, I’ll publish another post on my Lending Club and Prosper strategies. I’ll also break down my performance at least once a quarter.

Happy saving!

I don’t have tons of cash to spend but I’ve been putting a little bit into both Lending Club and Prosper. So far Lending Club seems a little better because Prosper doesn’t have that many Notes available at any one time but the returns on both have been great.

Just found your blog. Like the goal. I need to come up with something like that.

Hi Clay, I notice the same thing with Prosper in that there are just no loans available. I have had a little success with the Automated Quick Invest feature. Just today, it bought 2 for me. However, those were the first ones in weeks.

Hi Mr. 1500 days. Congratulation with your Peer to Peer Lending projects. Some years ago I had more money and was investing in a buddylending company called Trustbuddy. The company was declared bankrupt. Initially all money was lost because P2P lending does not have a guarantee like the banks. Luckily lenders created their own company to try to get their money back. Such things happen and can happen again. I have no money to spare now, but when I have I will not be afraid to lend out money again with P2P. The only thing is that one must not but money into such platforms that one can not afford to in worst case loose.