- Tyrion Lannister: l’m the captain of the ship, and if the ship goes down, l go with her.

- Lord Varys: That is good to hear. Though l’m sure many captains say the same while their ship is afloat.

Keep Calm

The markets have had an interesting couple of weeks. And by interesting, I mean bad:

But how bad is it really? If you pay attention to the media, you’d think that the end is near:

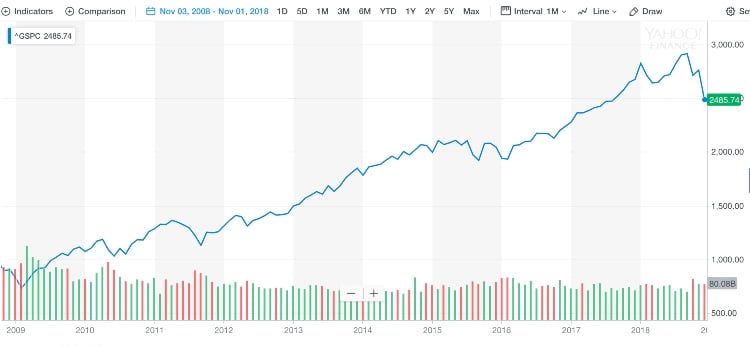

Take a step back from the edge and realize that despite all of the noise, the S&P 500 is back to where it was about 14 months ago. Contrast this with March 2009 when the index hit a low of 666, a number it hadn’t seen since 1996 (13 years!). And the most recent fall comes after a market that’s been charging upward for almost 10 years. In this perspective, it’s much less scary:

But, we still need to talk about how to prepare the mind for bad weather.

Storm Preparations

When is the best time to prepare for the following events?:

- hurricane

- divorce

- old age

Hint: It’s not when the storm comes or your spouse walks out on you.

The time to prepare for shitstorms is when skies are clear and sunny. You don’t buy home insurance in a hurricane or negotiate terms of separation in the middle of a bitter battle. You don’t wait until you’re old and grey to eat well and exercise. The same goes for money.

The best time to plan for a downturn is when markets are happy and healthy. Consider the following:

- How would a 30% drop in the S&P change your financial plan? Would it make you crazy with anxiety?

- Are you the type of person who wants two years of cash on hand to ride out storms or are you OK with an emergency fund of $0?

- If the market experienced a couple bad years, would you stay afloat?

- Bullet points are a strong indicator of lazy writing.

While I have no idea where the market is going, keep in mind:

- Investing is a long-term game. Over time, productivity gains and population growth grow economies which grow investment portfolios. But in the short-term, the markets are subject to the whims of politicians and geopolitical events.

- Building on the above, when I put money into the stock market, I expect it to be there for at least a decade. For more on the topic, check out Mr. Collins excellent Stock Series and/or book.

- Despite the recent market fireworks, 2019 could be much more chaotic. The trade war is only on hiatus. The North Korean nuclear issue hasn’t been resolved and is actually worse. Then there is American politics… Mr. Market doesn’t like uncertainty.

- Timing the market is very difficult. Don’t forget that you have to be right twice; it doesn’t do any good if you sell at the top, but fail to get back in at the bottom.

- Economic cycles are natural. Nothing goes up forever. They don’t go down forever either.

- Yes, more bullet points; more lazy writing.

- And on the topic of lazy writing, semicolons are another strong indicator.

Think long and hard about your plan before the market takes a big, steaming dump. The dump WILL happen and it won’t be comfortable, but it will be easier if you’ve set your mind right before it happens.

Keep Calm And Invest On

I had some money laying around that I was saving for a real estate deal. Instead, I threw some of it into the markets on 12/20:

I have another $30,000 in cash that I’ll throw into the fire if markets drop another 10%. Bring it on

When the Great Recession kicked my portfolio in the groin, I freaked out. I cut my 401(k) contribution and didn’t look at any of my portfolio balances for years.

Now, I’m in a different place. I know that no matter what the markets do now, there is a strong probability that they’ll be higher in a decade. I lose zero sleep when Mr. Market has a hissy fit. Instead, I welcome the drops by putting more dollars to work.

When the clock turns over to 2019, Mrs. 1500 and I will resume contributions into our 401(k) plans. If markets get really bad, we’ll throw some more after-tax money into the fire too.

If you’re investing for the long-term, I hope that you’re continuing to contribute money to the markets. The time to go shopping is when everything in the store is on sale. This is no different for the stock market.

Having been fully in vested in the 2000 and 2008 crashes, like you said – this ain’t nuthin’. It’s just a minor sale.

Happy New Year dude!

Retired people generally don’t have new money to put into the markets or their 401K, unless they are trying to time the markets. They just have to take what the market gives and depend on asset allocation.

Yep. I’m fortunate here.

But, I wouldn’t say that retired people don’t have to worry about investing money either. Many have more income than they can spend from dividends, deferred compensation plans, required minimum distributions, etc.

I think if someone early retired with a plan to withdraw 3-4% for living expenses, they are not going to have any leftover dividends for new investments, nor any RMDs. Not too many early retirees have def comp.

My boring, dollar-cost averaging monthly investments continue on despite the storm clouds…..and I just sunk some cash I had laying around into some high dividend-producing stock on sale, so maybe I’ll also get some growth mixed in if the stock market rebounds.

I am convicted by the following statements:

• Bullet points are a strong indicator of lazy writing – I thought I was just being efficient….

• Semicolons are another strong indicator; really?

As counter-intuitive as it may sound, bad returns today are good for our future money. It’s not easy to invest in market downturns, but it’s what separates the professional investors from the rest.

Great post, carry on!

Michael from Foxy Monkey recently posted…Why a stock market crash is actually good for you

We will drop our Roth IRA money on January 2nd as we do every year. The market can go up or down at any time. Long term it goes up though long term could be 6 months or thirty years. No one knows anything about the future so invest accordingly.

I am fully invested, so I do not like December drops.

401k was maxed out. Roths maxed out. HSA filled up. I did re-balance as we were 3% off between stocks/bonds. I managed to buy $500 2 times after the Christmas spend-a-whammy-shop-a-riffice-time.

2019 should be interesting. Will the drops continue or find some stabilization ground? Nobody knows.

I follow a number of blogs and the “December Updates” will not be pretty. Really the first sizeable drops since 2009ish. Many blogs started after this point.

It happens and those $100k, $200k+ dips will come and go. Happy new year!

Look on the bright side. A December drop can lead into a January drop or at least it’s a low. All your account maximums for 2019 reset to $0. Time to max them all out again at a discount.

i’m glad i raised cash back in october from 3% to 17% of the portfolio. it was something i was meaning to do and writing about it and our proximity to retirement was the big driver of that. how could i put it on the page and not follow through? i’ll take another look later this week and if the stocks have shrunk to make the cash balance over 20% i’ll “rebalance” to maybe 18% and keep doing that if stocks keep going down. it feels good to have 4-5 years of living costs in cash just in case.

all that being said it sucks to see over a 100k haircut in a few months.

freddy smidlap recently posted…A Smidlap Christmas

For the first time ever last night I invested my entire paycheck into the market. I was more than happy to do it, especially given the current climate. These days I’m way more worried about making sure the Personal Pan Pizza is eating enough and getting sleep (or more like us getting sleep) 🙂

• Bullet points are a strong indicator of lazy writing.

Jeez Carl, I almost spit out my coffee laughing

What about the liberal use of graphs, charts, and pasted gifs; fills up a lot of page space, eh…? 🙂

Best wishes for 2019 to the 1500 family and readers!

“You don’t wait until you’re old and grey to eat well and exercise.”

*Wait.

*What?

*That is my; plan

*Oh, and

*thanks for

*the link

*s

As I navigate my ship to the retirement waters, this downturn is just what I needed. I am converting my remaining IRA’s to Roth IRA’s to take advantage of the downturn. As part of my planning, I use a tax calculator to determine how much I can convert to keep me in my budget. I have budget $20k per year in federal taxes and as the market sinks I can convert more shares to Roth. I have $130K left to convert and I will do so over the next 5 years to have all accounts completely converted before I retire.

People ask why I am converting now. 1) More shares can be converted, 2) I have the cash to pay the taxes now, 3) It will allow me to take SS earlier and not have any of my SS taxed. 4) I firmly believe that with the new socialism that is hitting Washington that taxes will only be going up.

Same as you!

I had been holding on to some cash, anticipating some drops, so I took that opportunity to buy when the market took that dive. I’m going to keep gathering cash throughout this year and stay on the lookout for any more drops. We’re lucky that at the start of this recession (well, whenever it decides to start), we’re still working and our debt is limited to a couple mortgages. I started tracking money and blogging in 2006 but didn’t have real assets until about 2008. I’m hoping our next decade starting from now will see the same level of exponential growth we had in the last one.

Revanche @ A Gai Shan Life recently posted…2018 Goals: How’d we do?

Investing I think is very important in everyone’s life. Your article is really very good and very helpful too.

nick recently posted…5 Reasons Your Property May Not Be Selling (& How To Fix it)

Investing is key in a business oriented person’s life.Putting money and focus on something you want requires patience since it builds with time.Make the right investment to ensure good returns which provide more opportunities to invest further.No matter how small it is,try investing in profitable things.

Emily Brown recently posted…10 Money Saving Tips That Will Help You Get Through the Month

Investing on the right place is the right move and pretty good tips up there it might be very helpful for people who are retired and thinking on how to invest their retirement funds.

Great thoughts. Stock market crashes are just part and parcel of an economic cycle. Stay the course is the way to go. In fact for the past 90 years the stock market is still on uptrend despite countless stock market crashes. https://www.macrotrends.net/2324/sp-500-historical-chart-data

Desmond Mar recently posted…How to Calculate Your Net Worth (And Why it Matters)