Sometime in 2014, our little family of 4 decided that we’d spend the holidays alone this year. Everyone we know is scattered and we wanted to sit back after a hectic 2014 and relax for a bit.

In the fall, Mrs. 1500’s family announced that they were coming by us for the holidays. Ummm, OK, at least we don’t have to go anywhere.

At the same time, my mother started dropping guilt bombs on us left and right:

It would be so nice to see the grandchildren for the holidays.

It won’t be the same without you.

Your sisters will be here….

I caved. All of a sudden, we had lots and lots of plans.

Mrs. 1500’s family came out for about 5 days. Luckily, the family feuds were few and far between. One particularly obnoxious member of the clan continued with her obnoxious ways, but she was easy to ignore. However, her children did bring a nasty virus and left it with us. Thanks.

We then drove to Las Vegas to see my folks. There were some treacherous conditions in the mountains, but the trip was otherwise uneventful. From there, we drove to Phoenix to see some friends. Finally, we went down to Tucson to visit with more family.

Tucson was a highlight because the city has an awesome airplane museum and Mrs. 1500’s cousin is a wicked good cook. The airplane museum has an SR-71 and an A-10 Warthog, two planes I am especially fond of. And then there was the cooking.

If you’ve never had real mole sauce, it is one of life’s great gastronomic treats. I’m not sure I’ve ever put anything so delicious in my mouth. This rare treat caused me to eat at least 10 tacos (I lost count). In one case, I just filled up the taco shell with the mole and nothing else. Anyway, I didn’t feel so hot after gorging myself, but it was totally worth it and I’d do it again in a second.

Why am I telling you all of this? I have no idea. Oh, I know why; it’s an excuse. We arrived home from all of this road tripping/ airplane drooling/ mole eating and I had to go back to work the next day. All of the blog-work I had planned to do on my week off was flushed down the potty. So next week, we return to our normally scheduled posting schedule. However, I do need to tell you about how we did in December.

My main goal is to build a portfolio of $1,000,000 in 1500 days with no debt*, starting from 1/1/2013. Every month, I provide an update on my status. My goal for 2014 is to get my portfolio up to $768,536. Because we saw exceptional returns in 2013, I have accomplished this goal as well as my goal for the end of 2015.

Whoah, where did the time go? Bye bye 2014, hello 2015!

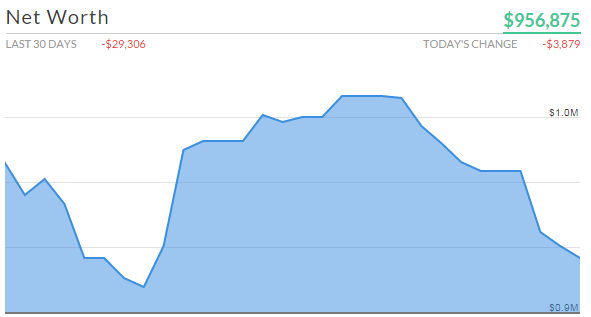

December was a down month. I started the month at $1,002,836 and ended at $987,351 for a loss of 1.5%. (Since initially joining the Double-Comma Club, I’ve been kicked out 3 times. I’ve never made it even a week.) I underperformed the S&P 500 which saw a smaller loss of about .34%.

In most months, Apple makes or breaks my portfolio. December was no different. Apple dropped like a… well Apple, and kicked my portfolio in its apples. Hopefully the AAPL doesn’t sour further when earnings are announced at the end of January.

Here are the numbers as of 12/31/2014:

2014

- Days elapsed: 365

- Days remaining: 0

- 2014 gains: $117,716

- Left to go (2014): Goal accomplished!

Since the start (1/1/2013)

- Days elapsed: 730

- Days remaining: 670

- Gains since 1/1/2013: $401,308

- Needed for $1,000,000 (investments and cash only): $12,649

- Net worth***: $1,187,351

Back to saving

Back to saving

My 2014 was very good, but it could have been a whole lot better. The investment part of my portfolio went from 820K to 987K for a gain of about 17%. Woo! On the other hand, we blew about 50K on home improvements. We currently have just $2,000 in cash. Not good. In this low rate environment, I’m not a big fan of cash, but $2,000 is really pushing it.

Since our remodeling expenses are mostly in the rear-view mirror, I look forward to building up the pile a bit. Because of my new work situation, I should be able to put lots of money into the 401k too.

The second to last stock I’ll ever buy

Lending Club IPO’d in December and we purchased 500 shares at the IPO price of $15. The stock took off like a rocket and now sits at about $23. What does that mean? Pretty much nothing.

While I’ve taken some ridiculous chances on stocks in the past, I’ll now only consider buying a stock if I’m confident that the company will be much stronger 10 years from now. Of course, it would be silly to buy a stock if I didn’t also feel that it would outperform the S&P 500 index. Beating the indices is just about impossible unless your name is Warren Buffett, so don’t follow my lead.

However, I really like Lending Club. I’ve been following the company for years and am a big believer in their business model and leadership. They have a product that fills a void (low interest, uncollateralized loans), much like the iPhone filled the smart phone void when it stormed into the market in 2007.

What is the last stock I’ll ever buy then? If I ever buy anything else, it will be more Berkshire Hathaway.

Where do we go now?

Anyone in the stock market has had a very good run lately. The party can’t go on without taking a breather every once in a while, but when that pause will happen is ridiculous to predict. On the downside, much of the world is struggling economically. However, the US has somehow managed to keep its head above water as economic indicators continue to improve.

As for me, I’m going to keep throwing money in the direction of Mr. Market. One thing I’ve been thinking a lot about lately though is that only 1% of my portfolio is in bonds. The rest is in stocks (some pure stocks, but mostly funds). While I consider myself to be an aggressive investor and very comfortable with risk, perhaps more of my future money should be directed to bonds. Thoughts?

*I still owe something like $120,000 on my mortgage. Because I have a low rate, I firmly believe in not paying it off. My compromise is to have enough money put away to pay off the mortgage at time of retirement. So, to retire today, I would need about $1,120,000.

**This is an affiliate link. If you sign up, the blog makes a little bit of money and I can afford to carry on with ridiculous home improvements and fart jokes.miss any fart jokes, would you? I didn’t think so. With that out of the way, I would never recommend anything I didn’t use myself and completely believe in. Personal Capital is totally free and and awesome way to keep watch over your investments. It’s worth it for the fee analyzer alone.

***The numbers on the right side of the page only reflect my investments and cash. Net worth includes, but is not limited too:

- Home equity

- Cars

- Bicycles

- Paint: Mrs. 1500 is in charge of paint. Recently, I was cleaning up and moved it all to another part of the house. It was at this time that I realized just how much we have. I have no idea what dastardly plans she has for all of this.

Oooh! Did you walk around the airplane graveyard while you were in Tucson, too? Weather would have been nice for it this time of year. =)

As for bonds, it’s been a while since I looked at our exact ratio, but I think we’re around 15%. Why? Not sure entirely… perhaps we need to revisit why we made that decision a while back. =)

Mrs. Pop @ Planting Our Pennies recently posted…The 80/20 Rule At Work In Our Kitchen

I would have loved to go to this too, but just ran out of time. There are a lot of cool things to do down there. Next time, I’m going to plan for a week at least.

15% seems smart. You won’t take as big of a hit when the stock market gets pummeled. This is the kind of thing I think about every single day. I need more hobbies perhaps!

Most of the stories I hear about holiday travel, family and kids always seem to involve a virus of some sort. Sometimes, that makes me happy my kids don’t have cousins!

We are low on bonds also – but mostly because I’ve been feeling risky and since we are both still employed we can handle the risk, since we are still playing the long -game. Also, I don’t understand bonds as well as I do stocks – but they are something I want to get more comfortable with in the next year or two, as I realize they will need to play a bigger part of my portfolio once I pull the plug on the job in a few years.

Mrs SSC recently posted…Early retirement fail

Ha, children == viruses. Before having children, I never got sick. Now, the kids bring home all kinds of nasty things…

I’m still torn about bonds. The run in equities can’t go on forever, but many smart folks have pointed out that a portfolio focused on stocks has historically beaten a bond heavy portfolio. I think that my goal will be to have a couple years of spending money in bonds or cash. No more. I could then dig into that pile if the equity markets bombed.

Everytime I read your blog I can’t believe the ability you have to break down your budget to the penny like this. I am beyond conservative with my money and really need to tear a couple of pages out of your book. It is a privilege to go on vacation with your family and not have to worry about money when you get back home. Looking forward to following your journey.

Petrish @ Debt Free Martini recently posted…5 Financial Myths to Ignore

Thanks for the kind comments Petrish! Worrying about money is the absolute worst. Can’t stand it.

*cough* *Diversify* *cough* 🙂

You’ve got to plan on a solid way to start leaving that AAPL position! I can think of a couple of ways, and the only new one I’d add is to just donate them to me. Much easier to pull that trigger than stop-losses, covered calls, etc.

Either way, good to see that 2015 will be a year where cash flow is better. Hope the new employment situation works out well and you can leverage your “independence” and take advantage of being a business owner through some deductions and creativity.

Ha, I can’t argue with that. Yesterday, I set some trailing stop-loss orders on $AAPL. I’m also going to look into covered calls as you previously suggested. I’m torn though because I think Apple is going to have a very strong 2015. On vacation, I noticed friggin’ iPhone 6 everywhere. Apple is selling loads and loads of these things.

The business thing is working out well so far and I have big plans: Berkshire meeting: write off. FinCon: write off. Toilet paper for home office bathroom: write off. Just kidding on that last one. Maybe.

Can’t argue with that?!?! Does that mean I’m getting shares in the mail? Hooray!! 🙂

TP… *flips IRS guidelines* … doesn’t seem to be excluded. Consider it good to go as office expense. Done and done. Same for the stamps to send my cash from the AAPL shares.

writing2reality recently posted…Trades – December No-Cost Dividend Growth Portfolio Purchases

Shares in the mail! Yes, they are on their way. They should show up any day, but don’t hold your breath!

I go through a lot of TP. Hopefully I don’t raise a red flag. It would be good news though: “Man audited for excess pooping.”

There are only a few certain things in life…death, taxes…mothers dropping guilt bombs =) Glad to see you’re almost to your goal. How were you invited to buy Lending Club IPO shares? I guess I missed out since I have only a small amount with them.

Andrew@LivingRichCheaply recently posted…Live For Today

Lenders who had been with LC were given the opportunity to buy shares. Very cool of LC to do that. I love the company.

Any advice on how to dodge the guilt bombs?!?

Ooo…paint. And maybe you can educate us on buying muni’s. I’d be interested in that!

Elroy recently posted…Israel – Intro

Ha, I know nothing about municipal bonds. I was thinking more along the lines of this: https://personal.vanguard.com/us/funds/snapshot?FundId=0084&FundIntExt=INT

I don’t think I’d be a very good bond investor though. As soon as the market crashed, I’d be moving it all back to equities…

Wouldn’t the opposite be true about the market crashing and bond performance?

In other news, 5 yr CD’s are yielding better than the total bond fund you link to, sans inflation risk and all the other risk bonds can have [I don’t know the terms]. To pique my interest in today’s market, it would have to be LOW risk and 3.5%-4%. But, I don’t see that happening […] so I crank down my risk a bit and just roll with CD’s. Of course, depending on your portfolio, you may want step down risk from equities, but not quite the high grade of bonds VBTLX […] all depends on you! Good luck.

Elroy recently posted…Israel – Intro

Sure, bond performance would improve if equities crashed. However, long term, I believe that stocks outperform bonds. So, I’d probably move money over in a recession. Easier said than done. See Mrs. Frugalwood’s comment about rebalancing below.

I get the principles of rebalancing. I don’t get how one could not use CD’s in this practice?

Elroy recently posted…Israel – Intro

Super bummed we couldn’t get a beer when you were in Phx. Stupid holidays. We’ll make it happen one of these days.

Glad you made some good money on the IPO: pretty great result, IMO. Maybe you’ve got some Buffet in you? I’m not keeping track, but a lot of your single stock picks have beaten the S&P….

Done by Forty recently posted…Playing with My Emotions

Yeah, next time no matter what. There is so much I want to see and do in Arizona that we’re going to plan for a much longer visit next time.

I’ve beaten the indices with everything I’ve bought (Google in 2004, Apple in 2007 and Facebook in 2012). However, the true measure is decades…

I’m excited to hear about the plans for house flipping, might just quit your day job?

Even Steven recently posted…Act Like Your Grandpa and Grandma in 2015

I really enjoy the flipping. The issue is so do lots of other people where we live, so good candidates are hard to come by. We sure are going to try though!

I was there for a short period of time trying to find a house to flip, many offers were made and it just didn’t work out that way. The family money(the stress would have been crazy) ended up going towards a rental in Florida that we are not apart of, let’s just say I’m happy the way things worked out.

Even Steven recently posted…Act Like Your Grandpa and Grandma in 2015

We’re heavily invested in equities as well with very little bond. I’m comfortable with that considering our time line is very long.

Tawcan recently posted…Happiness is not a fish you can catch

I’m a bit worried now because my timeline isn’t so long. Perhaps if I had a couple years cash in the bank to hold me over in the event of a crash I’d be more comfortable. That is almost the same thing as bonds though. Hmmmm…

Perhaps using P2P Lending as a potential substitute for bonds/massive cash account? If you invested in all A-B grade, 36-month notes, you’d be turning over cash quite quickly. If you built up to $100,000+ in P2P, than, you’d conceivably get cash out at a $3k per month if you halted reinvestment. Certainly would scale with inflation for as long as you kept investing it.

My thought would be 8-12 months of living expenses in cash, two years in P2P, rest however you see fit. Keep your cash in line as needed from your equities as your normal withdrawal rate and P2p as the cash flow to protect mid-term cash needs above and beyond the emergency reserves.

Of course if you’re flipping houses, you’ll likely have a substantial cash stack anyways to maintain some liquidity for that process. Plenty of concepts out there, just have to be creative and find the one that works for you!

writing2reality recently posted…Trades – December No-Cost Dividend Growth Portfolio Purchases

I think P2P lending for a reserve is a great idea. With 100K, three years of income would go a long way to making my way out of a rough patch.

The one thing I wonder about is how P2P numbers will be affected by a recession. If the market craters, people will lose jobs and the first thing they’ll stop paying is uncollateralized debt. I’d bet returns would suffer by at least a couple percentage points.

This is true, returns would dip – but if you’re in the super prime category (AA-B), the dip will likely be slight. I’d imagine even getting a return on principle and a couple of percentage points of positive net interest would still be fairly reasonable.

writing2reality recently posted…Trades – December No-Cost Dividend Growth Portfolio Purchases

I guess the answer to your investing questions depends on where you want to go from here. Do you just want to hang around the entrance to the double comma club and start living off some of that income, or do you want to keep growing it as best you can towards another target?

If you want a more stable portfolio, then I think diversifying into bonds isn’t a bad idea as Writing 2 Reality mentioned. The other option is to put some of those funds into some rock solid dividend stocks, or a dividend Index or Motif or something similar. This is probably what I’ll start doing once I hit the million, and will probably stay 100% equities all the way there, although there’s a good chance that once I get there I’ll want to try and keep growing it aggressively…

Jason@Islands of Investing recently posted…The plan for 2015 – Islands of Investing Income Increase Initiatives!

I go back and forth. For example, if I had 2 million in the can, I could easily survive any rough patch. Market goes down by half? Not a big deal.

However, I’m not at 2 million, so perhaps some of the money would be better in safer investments.

We only hold 10% in Bonds.

Here’s how I mentally justify that when we’re looking at pulling the retirement trigger in just a couple of years: Add in your cash stash to get a true “non-equity” percentage.

We have a decent amount of cash flowing through our accounts at any one time. Some of it destined to be invested on schedule, some of it being earmarked for other things (like potential homestead buying).

I see the bond allocation in a portfolio as “dry powder” to be used when the markets are down and your yearly rebalancing will cause you to buy into a cheaper market. And the inverse when stocks are expensive. I just rebalanced our stuff the other day and sold a decent amount of Total Market Index to buy some Bond Index in order to get back to the 90/10 intended split.

But if there was a major correction, I’d be happy to use some of our normal cashflow to buy cheap(er) equities. That cashflow (and our liquid cash on hand) serves as a bond analogue. And with the rates that bonds get these days… there’s not much of a difference in returns. 🙂

Mr. Frugalwoods recently posted…Frugal Hound Sniffs: Eyes On The Dollar

I like the “powder keg” idea a lot. When markets crash, you’ll be moving money in the opposite direction; bonds back to stocks.

What is your rebalancing trigger? Do you have a threshold or certain time of the year when you do it?

I’d also like to know where the homestead stash sits. It would be killing me to have a substantial amount of money in case for the past 2 years. On the other hand, it’s not wise to keep money that you’ll need soon in stocks…

It’s funny how stuff always piles up around the holidays. You can have the best of intentions of taking it easy and staying put, but something always seems to come up. My wife and I have the blessing/curse of both being from the same town, so the good thing is that during the holidays is that we can see everyone. The bad thing is that we have to see everyone. This year the wife also got hit by the flu bug at the holidays and brought it home, but I seem to have escaped it.

Also, the A-10 is one bad a$$ airplane. We had them for support on a few missions when I was in the Army. Man, the sound that main gun makes is awesome. If I were a bad guy and I hear that BBRAAAAAAP! sound I’d crap my pants.

Frugal Buckeye recently posted…Go Bucks!

I’ve listened to the sound of that gun on YouTube! I wouldn’t want to be in the enemy tank when the Wart Hog shows up; that’s for sure.

Having family near would be nice. I loved family gatherings as a kid. Now, we’rell all spread out and I get a bit sad sometimes that my children only get to see aunts, uncles, grandparents, etc. a couple times per year. On the other hand, there are times when I really appreciate all of those miles between us.

There’s nothing quite like being close to family. I’m sure there will be days when we regret it, but the gravitational pull is really working on us moving back there.

The miles are nice when it comes around to a holiday that you really don’t want to spend as a hectic trip, then you can pull out the ole sorry we’ve gotta chill at home this one.

Frugal Buckeye recently posted…Go Bucks!

You are doing a great job monitoring your income and outflow, but doing a lot of investing in individual stocks is dangerous. Even Warren Buffet gives this advice. He recommends Vanguard indexed mutual funds, and has a specific recommendation here: http://www.wsj.com/articles/investors-pour-into-vanguard-eschewing-stock-pickers-1408579101

I couldn’t agree with you more. While I’ve done well at stock picking, I don’t do it much anymore. In fact, I even called myself out here: https://www.1500days.com/thursday-rant-1500-portfolio-part-3-no-empire-lasts-forever/

The main reason I still have so much money in stocks is because I don’t to take the capital gains hit. If I wait until I’m retired in a couple of years, I could rebalance and not get a huge tax bill.

I realize that I’m playing with fire. I do have a big trailing stop loss order on Apple. I will throw another one on facebook later this year. So, I expect my diversification to start earlier than retirement. And if it doesn’t that is more money in the bank.

Yes, your post from August is excellent. Everyone should read that. For cost-wise living, sometimes taken to an extreme, along with good investing advice (albeit Vanguard-centric) you could have a look here http://www.bogleheads.org. You might find some useful thinking here. There have been some Lending Club and Prosper threads at Bogleheads too.

Hey Mr. 1500. I wonder how you got 500 shares of Lending Club at the IPO. I’ve been an avid lender on the site for 3 years and also got in on the IPO. I’m guessing you and your wife both bought 250, the limit. When I signed up for the IPO, I asked for 150 shares, but was only sold 100. I figured everyone ended up getting 100 at the most because there was so much interest. Any idea?

Norm recently posted…Our Travels Using Frequent Flyer Miles: Introduction

Hey Norm-

Yes, you’re absolutely correct. The wife has an account too and we both asked for 350 shares, which netted us 250 each for 500.

Glad you made it through the Holiday travels and visits with only minor nuisances and great mole.

The best book I’ve read on investing is “The Four Pillars of Investing” by William Bernstein. He’s a Ben Graham follower, like Buffett. He goes through a good bit of analysis and argues that you should hold at least 20% bonds even as a high-risk investor. According to him, that last 20% of stocks doesn’t give much more long-term return (vs bonds) but adds a good bit of risk.

Sir Salty recently posted…Wilderness (Re)discovered

Thanks Sir NACL for the input. I’ll add that to my list and take that advice under consideration. I know I’m playing it way too risky now (in more ways that just this), so one of my goals for 2015 will be to make some moves…

It’s worked for you so I’m not judging or anything. I’m in the same boat – only I’m way heavy in real estate and will be trying to diversify out of it a bit in the next two years.

Sir Salty recently posted…Wilderness (Re)discovered

We have 20% bonds, and are looking at slowly moving that up to 30% over the next 5-7 years. I’m aggressive, Dad is not, so we compromised with slightly higher bond percentage. The upside to that is we’re not losing as much as the S&P500 has over the last few days (we’re still losing, but not as much). The bonds also throw off “dividends” in the form of interest payments – but they’re classified as ordinary income for tax purposes. I rebalance when anything gets out of whack by 3% or more (I have a nice Google Spreadsheet that keeps track of that for me).

Mom @ Three is Plenty recently posted…Detailed Financial Picture – January 2015

The market has one hell of a run these past 6 years. With most global markets struggling around the world, it is amazing that the US has been able to continue its forward momentum. However I think October of last year was the first sign of weakness that showed up in the form of very high volatility.

The fed announced as expected the end to its bond buying program. The S&P 500 did correct by about 10% (based on its intra-day low), only to bounce back up almost 14% in a few weeks period.

Oil has been the first asset class to have a serious and sustained correction. To me this is where opportunity to get long exists. I fundamentally believe in buying into weakness. Plus as a premium seller, high volatility makes for some really fat premiums to sell puts (equivalent of getting long the stock, but with less risk and a more favorable entry price).

I don’t know how much you track bonds, but they are at all time highs with interest rates at all-time lows. I believe that interest rates will likely stay very low for a long time, but I don’t think they can go much lower. This means that there is a lot of downside risk in buying bonds. If you consider the inverse relationship between bonds and interest rates, bonds probably have the most downside risk of any asset class at the moment, followed by the S&P 500.

I know with lower rates you are against paying off your mortgage. However you probably also don’t want to buy the top in bonds. Given that you are interested or okay with the interest rate that say a 20-year bond would return…something like 2.5% on the ETF TLT…then you may want to reconsider that position. You can likely match or exceed that rate of return by putting it towards the principal of your remaining $120K mortgage.

That’s what I am doing. Since I think it is going to be a long, long, long time before the fed is going to be able to raise rates and with markets at all-time highs, I have significantly reduced my long exposure to the market and have put in place a 7-year plan to pay off the mortgage on my primary residence.

I am actually long oil related equities via the USO and OIH ETF’s. Slightly short the S&P 500 as a hedge and short TLT (20-year bond ETF).

Looking forward to following your 1,500 day journey and where you decide to deploy capital.

Cheers!

Gen Y Finance Guy recently posted…The Mortgage Snowball Strategy To Pay Your Mortgage Off In 5-7 Years

I’ve never thought about bonds versus a mortgage like that, but it makes a whole lot of sense.

I did end up moving some of my assets to bonds, but those holdings are still minimal at less that 5% of my portfolio. However, I’m less than excited about it, especially after reading what you wrote.

My goal is to get rid of bonds completely in favor of peer lending (Prosper and Lending Club). I’ve been on both from almost the start and have always done around 10%, despite not knowing what I’m doing.

So, I’d like to have 10% of my portfolio in peer lending. If I run into a rough spot, I can just stop reinvesting the money and collect $3,000/month for 3 years.

Finally, thank you for taking the time to write such a detailed and useful comment! Much appreciated.

What has your experience been with default rates on the peer to peer lending sites? Also what size loans do you give out. I think I remember reading that you can do loans as small as $25.

Lastly between Lending Club and Prosper, which do you prefer?

Cheers!

Gen Y Finance Guy recently posted…The Mortgage Snowball Strategy To Pay Your Mortgage Off In 5-7 Years