Some thoughts before we begin today’s Rant:

I’d rather take a chance and be free than stay chained to my desk in the name of safety.

I’d rather play with FIRE than live a conventional life.

If you ever see a Komodo dragon in the wild, run like hell.

The 4% Rule

If you’re going to quit the workforce early, I’ll bet that the 4% Rule is one of the cornerstones of your planning. If you’ve never heard of the 4% Rule, it refers to a study that was done to determine the maximum safe withdrawal rate in retirement over a 30 year time period. Basically, it states that if you can live off of 4% of your investments in the first year, you are ready to retire. I will spend $40,000 in my first year of retirement, so I need to accumulate $1,000,000 before I can tell my boss what to do with my job.

Mainstream Media Nonsense

If you read the mainstream media, you’ll notice that approximately 99.746% of the articles about the 4% Rule are negative. Here are some that I’ve read recently:

- Why you’ll go broke, catch an STD and live in a box if you abide by the 4% Rule

- Why dinosaurs will eat you if you follow the 4% Rule

- How the 4% Rule drove your spouse to Ashley Madison

- Why the 4% Rule keeps your husband from replacing the toilet paper roll and putting the seat down

- Why following the 4% Rule will cause the band KISS to reunite for the 736th time and play a concert in your backyard

I can’t seem to find links to any of these journalistic masterpieces now, but you get the picture; the mainstream media wants you to fear the 4% Rule.

Why you’ll probably be OK

I’m not an economist or a financial planner, but I play one on TV. Not really, but sometimes I play one here. In my amateur view, you should embrace the 4% Rule with open arms and an open mind. The 4% Rule is your friend and a good friend at that, not the one who borrows your tools permanently or flirts with your spouse when you’re not paying attention. But the one who brings good beer over* and helps with miserable projects.

The 4% Rule assumes no future income: If you live in America, Social Security will still be around. The same doomsayers who tell you that the 4% Rule is evil will also tell you that Social Security is doomed. This just isn’t the truth.

Social security is not without issues, but it’s a sacred cow that no lawmaker would ever let die. It will be diminished and politicians should be spanked for borrowing heavily from it, but it will still be there.

The 4% Rule only counts for 30 years, but your money will probably last much longer: The original study only assumed 30 years, but I’m here to tell you that chances are very good that your money will last much, much longer than that. Have a gander at the beautiful table below courtesy of the FIRE Simulator (cFIREsim). The scenario is based on my own situation; retiring at 43 with $1,000,000, buying the farm at 100 and starting with a withdrawal of $40,000 (4%) in my first year.

- I have an almost 90% chance of success! And I’ll tell you that I’m not 90% sure of many things in life. For one, I highly doubt I’ll live to be 100 (some day, I’ll tell you about all the times I’ve launched myself over my bicycle’s handlebars).

- In the best scenario, I end up with almost $36,000,000!! What on earth would I ever do with that (party in the 1500 backyard with

KISS, Van Halen!!)? - My average scenario leaves me with $10,000,000. No idea what I’d do with that either.

The 4% Rule isn’t failure proof: And neither is anything else. Despite your best attempts, all of the following are possible:

- Your child may end up working the carnival

- Your wife, who seemed perfect when you married her, may run off with a member of a KISS cover band

- You may get eaten by a Komodo dragon on your next trip to Indonesia

All of these scenarios are horrible, but also improbable.

The simple answer is to not be rigid:

- If your firstborn gains employment working the ferris wheel at the state fair, perhaps he wasn’t Ivy League material to begin with. Tell him you love him and that you’ll be there for him. Then, ask if you can get a ride on the house. Be thankful that he has a job and makes it out of your basement to go to work.

- If your spouse runs off on you with a faux member of KISS, go find someone better. Or put on some make-up and pick up a guitar: \m/ \m/

- If you’re attacked by a Komodo dragon… I’m sorry, but I’m running as fast as I can in the other direction. No thank you to any of that. I hope that the end is quick for you, but it probably won’t be.

Regarding the 4% Rule, if you are unfortunate enough to retire at one of the points in history where the stock market takes a huge dump the next day, just tweak your life a bit. If you’re frugal and get by on modest income, driving for Uber occasionally or renting a room through Airbnb can turn the 4% Rule into the 3.5% Rule, greatly increasing your chances for success. When I ran the 3.5% scenario in the FIRE Simulator, my success rate jumped to 100%.

I know that you’re not stupid, so in the rare case where the 4% Rule doesn’t go according to plan, you’ll find a way to deal with it.

If I were to nitpick the 4% Rule…

The 4% Rule is based on historical data from a time when economies, population growth and technology advanced rapidly (1925-1995). If I were to make an extremely amateur guess, the world will continue to progress, but perhaps not at the same blistering pace.

Do I care? Not really. If you think the same as me, perhaps you choose to live by the 3.8% Rule or retire when market valuations are low. Or just remember that you’ll get Social Security later on. No big deal. Move on now.

The risk that no one talks about

The haters will tell you that you’ll run out of money if you follow the 4% Rule. I’m concerned about the opposite. What if I have $10,000,000 in the bank when I’m 100? This will mean that I worked far too long and could have been living it up while I continued to slave away at my job.

I’d rather take a chance to be free than stay chained to my desk in the name of safety.

Komodo Dragon Dreams

Nothing is certain in life including your financial future. However, the 4% Rule gives us a solid framework to plan with.

Life is a bit of a game. If you’re lucky enough to have been born in a place with opportunity where hard work is rewarded, you can take your life in any direction you want. However, a large determiner of your success and well being can also be attributed to your attitude. You can choose to worry about scenarios that probably won’t come true or chase down your dreams.

I encourage you to strongly consider the latter.

I believe your dreams have a far greater chance of coming true.

And if you ever see a Komodo dragon, keep your distance.

For sane viewpoints on the 4% Rule, see the following:

- This one, from the Mustachefather, is the post that told me it was OK to retire early. My tipping point if you will.

- Here is another great take from Go Curry Cracker

- Last, but never least, please read what Jim Collins thinks

Hat tip to Go Curry Cracker and ThinkSaveRetire for inspiring this one. I was originally going to run something even worse today, Thanks fellow FI folks!

*Shout out to Denver E for sharing one of the best beers ever, just last night! Having a great beer is good. Have a great beer with a great friend is infinitely better.

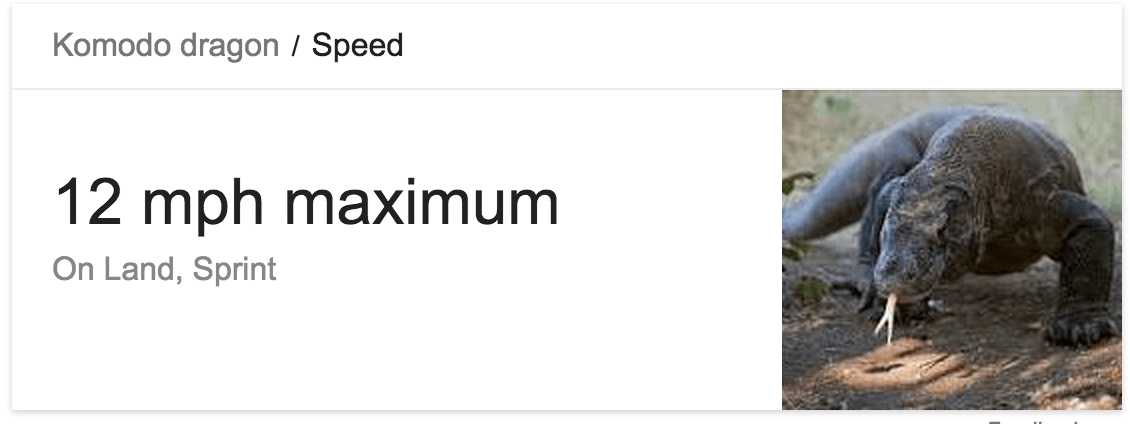

**Who says you don’t learn anything over here on 1500 Days? If you’re on Jeopardy and you win big because you know a Komodo dragon*** can run 12mph, I expect an acknowledgement. If nothing else, you’ll dazzle your friends and family this weekend with this fun piece of trivia.

***Damn, I can’t stop thinking about Komodo dragons now. There is even a Jurassic Park-like experience if you want to see them in their element and apparently, even yank on their tails. What could possibly go wrong?

That article on MMM was my first introduction to the 4% rule. It really opened my eyes to the possibilities of maybe not retiring early (I think I’ve missed that boat) but definitely retiring comfortably. And that’s why the mainstream media are so negative. It gives us a clear path and the motivation to get out of the rat race.

Oh, and I believe Komodo dragons can run pretty quickly. So best bet is to climb a tree! 🙂

diane @smartmoneysimplelife recently posted…How to Deal with Inbox Overload and Other Digital Clutter (without going crazy)

Ah, a tree does sound like a better bet! I think they’d be out of luck if you were able to get a foot off the ground. Hopefully, I’m never chased by a black bear and a Komodo dragon simultaneously.

MMM was the first one I read who really seemed to know what the heck he was talking about, especially going beyond 30 years.

One of my favorite hobbies is running simulations like yours. Lately, we have been trying to figure out what our risk tolerance is…. like are we happy if we succeed 85% of the time? Or do we need 95%? Honestly, I love the 4% rule – it is a good starting point…. but really, the whole key to ER is being flexible. Spend less for a few years when the market is down – or get a fun part-time job! I’ve realized with simulations that I can go by the 4% rule or a 3% guideline – and nothing is a 100% guarantee!

Mrs SSC recently posted…Stock Market Haiku

I love the simulations too! I could spend a whole day on that FIRE calculator site. Thanks bo-knows for putting together such an awesome tool!

One thing I’ve never understood about criticism of the 4% rule is they never allow wiggle room. Get a part time job, cut back on a few things or some combination of income generation/expense reduction will allow you to stay on track.

Also I tried a new beer last night, rum flavoured…

http://www.ab-inbev.co.uk/2014/03/discover-the-spirit-within-cubanisto/

so bad yet so very good!

It’s easier to be negative than positive I guess. Scary stories also get more clicks than ones that feature plastic dinosaurs.

Rum flavored beer? I have no idea whether that is a good idea, but I’m certainly willing to give it a try!

Hey 1500!

Thanks for the shout out, and I think that you said it best: “I’d rather take a chance to be free than stay chained to my desk in the name of safety.”

Because honestly, being chained to your desk isn’t necessarily safe either. Anything can happen in this world, and the goal is to find that point in our lives where we’re finally going to dive into the whole FREEDOM thing head first – based on a very high level of savings and living below your means. The saving and living part is easy.

Choosing to be free, ironically, tends to be the toughest.

My wife and I used the 4% rule as a baseline. We’re going to be living off of 3.5% at the beginning of our retirement and then re-evaluate as we progress through our retired lives. We have every reason to believe that we’ll be just fine because we are flexible and willing to adjust, as necessary.

Steve @ Think Save Retire recently posted…Your job vs. your work: Retirement police, listen up!

“Choosing to be free, ironically, tends to be the toughest.”

YES, totally true! The numbers are easy; it’s just getting past the emotions.

Thanks again for the inspiration!

I think a majority of the haters out there are jealous of people who retire early so they try to poo poo on the parade of early retirees dreams. My mom is about to retire, and even though she’s got no where near $1m in the bank, she’ll be living with us for free (in return for free child care) so her monthly income that’ll be only a little more than half of what you’ll be taking monthly (with SS and a small pension added to her retirement savings), will be totally fine for her since her expenses will be low monthly (as other family is also covering her cell phone and medicare part d payments). Heck, she probably won’t even need all the money, which I suspect in your case, might be the same too! How funny would it be in retirement if after you start taking your 4%, you don’t even use it all and start putting it in your online savings account? Frugality is a hard mindset to break.

also, in an unrelated note, have you ever had hard root beer? There’s a brewing company out of Chicago that makes Not Your Father’s Root Beer and even Coney Island Brewing Company is making a hard root beer now too. I heard InBev is developing one so that’s going to be the new trendy drink it seems. It’s delicious, although a little sweet. Perfect for an after-dinner root beer float.

I just had Not Your Father’s Root Beer for the first time on Monday. It was very good. A little syrup-y aftertaste but very good.

I did try it recently, although I don’t remember which one. I love root beer and I really love, well never mind… It was really great though. Coincidentally, I’ll be in Chicago in about 2 weeks, so I’m going to keep my eye out for this one.

I like the idea of extended family living together. Everyone wins in that situation as long as you all get along.

I suspect that I’ve already oversaved. I think I could have left work a while ago, but I tend to be really, really conservative about money. I’m almost there though.

What?! You’re not living if your not trying to wrestle a Komodo dragon! You show me a Komodo and I’ll show you the ultimate greatest hits of the croc hunter wrapped up in 5 minutes on a single wiley dragon! – BAM!

Oh, love the 4% analysis, our goal is to shoot for around 3%. Van Halen Rocks. Dr. Love will steal your wife. Damn those dinos! Can’t whoop the ass off a T-Rex…

Mr. Crackin’ recently posted…What if I had started now?

Hilarious! And, I’ll take you up on the challenge:

I have ordered the dragon. Who knew you could order these things off of Amazon. I got a small one (only an 8 footer) and it is supposed to arrive by way of drone (a very big one) on Saturday. Can you be over, say 8pm? For the opening fight, I’m going to wrestle the neighbors’ cat.

I just noticed the following on the Trinity study wiki page…

“Ironically, the 4% rule of thumb would, in many instances, mandate a more frugal level of retirement expenditures than a portfolio that was fully invested in government inflation-indexed bonds, such as U.S. Treasury Inflation Protected Securities (TIPS). As of mid-October 2008, Treasury Inflation Protected Securities (TIPS) boasted real yields of approximately 3%. A laddered, 100%-TIPS portfolio yielding 3% real would sustain a 5% safe withdrawal rate over a 30-year period. A 100%-TIPS portfolio yielding 3% real would not only be less volatile than a diversified, part-stock portfolio, but also safely sustain a much more generous level—25% more generous, in fact—of retirement expenditures than a diversified portfolio to which the “4% rule” was applied. While a 3% real TIPS yield is well above historical averages for TIPS yield, even a TIPS portfolio that yielded only 1.3% real would sustain a 4%, inflation-adjusted, safe withdrawal rate over a 30-year period.”

Um….what???

I’m glad you finished with “Um… what???”

The whole time I was reading this, I thought you were building up to throwing something in my face! I have no idea what the hell they’re talking about either.

I’m glad I’m not the only one who noticed all the doom and gloom articles about the 4% rule. Some of the articles did make valid points but as you say, flexibility is the key to success. That and good health. I imagine health expenses can really eat into your nest egg.

Yeah, a health issue could kill you. We’re on the ACA and the annual deductible is 10K. Two or three years of paying that would be painful.

It’s all doom and gloom. The way I look at it is you can concentrate on the 5% chance that you will fail or the 95% chance that you’ll have a glorious life, free of bosses and 50 hour workweeks. I’d rather take the 95%.

I’m a firm supporter of the 4% rule as well. It’ not like you’re going to enter retirement withdrawing 4% at suddenly look in your account and your savings are gone! If economic downturns or other things arise, you will have time to look at your portfolio, adjust your lifestyle or make other changes to accommodate your retirement.

Plus, by retirement you may not be quick enough to outrun a Komodo dragon…

Dane Hinson recently posted…Investing is a Long-Term Game

I better get my butt over to Indonesia while I still can run! Crap, I just Googled it and they can run 12mph. I’m a goner at any age.

Flexibility is key! If markets drop 25% in a year, I sure hope you have cash reserves or flexible expenses or drum up an income source so that you don’t have to pull 4% that year. If you follow the plan rigidly, that’s when you’ll run into issues. I don’t ever see myself NEVER earning income again once I reach FI. If the stock market tanks, maybe I’ll move to Mexico for a year 🙂

Fervent Finance recently posted…Why CPAs Are Terrible With Their Finances

“Flexibility is key! If markets drop 25% in a year, I sure hope you have cash reserves or flexible expenses or drum up an income source so that you don’t have to pull 4% that year.”

EXACTLY! This is my plan actually. I’d like to have 50-100K in cash at time of retirement. If markets are flying high like now, I’ll draw at least 40K/year. If they are in the dumps, I’ll turn on the cash spigot. Problem solved.

Can I keep a Komodo dragon as a pet? What would the neighbors say?

I think that would depend upon whether or not they can run 13+ mph . . . or have exceptional tree climbing abilities.

I have neither! I couldn’t outclimb an elephant and can barely outrun a sloth. Trip to Indonesia is cancelled! So are plans for the pet dragon.

Yeah, that’s the tricky thing about the 4% rule. It assumes ZERO income. I used to work with a guy who ran a public housing development and needed to check people’s income to see how much assistance they’d get, and he’d say, “It doesn’t matter what they report, nobody has zero income.” There’s always something. I think you’d have to really try to earn absolutely no income.

Whenever I run the numbers, I get to include a pension that kicks in at age 55. But it makes a huge difference if you include ANY income in retirement. Like in your example, if you’re spending $40k out of $1M, but between you and your spouse you make a paltry $10,000 doing something, anything that you enjoy, you’re taking 3%, not 4% out of investments. Which is a HUGE difference, all due just to that $10k income.

Norm recently posted…Cost Per Serving: Bittersweet Chocolate Tart with Candied Oranges

“Which is a HUGE difference, all due just to that $10k income.”

Yeah! That is why I think the key to the whole thing is being frugal. If you can live on a modest income, it takes very little to move the needle.

For me, if I ramp up the monetization, this blog could probably bring in more that $6000/year which would almost guarantee me success.

I am incredibly pleased that I won’t get the clap. I thought Mr. Crackin’ was the only one who could assure me of this but if you say so….. Awesome post as always!

Mrs. Crackin’ the Whip recently posted…What if I had started now?

You won’t get the clap! And I have even more good news; as the 37,161 commentor here on 1500 Days, you’ve won a Komodo dragon! Do you have a feral cat population in your ‘hood? Not anymore. Do you have a problem with pushy salespeople at your door? One look at that ferocious dragon and they’ll run for the hills!

Mmmm…

I didn’t think you noticed me flirting with your wife….

Moving on…

Thanks for the link to my take on the 4% rule. This laugh-out-loud funny post of yours is now an addendum there. Thanks for brightening my day. And say hi to…

…ah, never mind…

jlcollinsnh recently posted…Mr. Market’s Wild Ride

Ding! Ding!! Ding!!! Mr. Collins wins the Comment of the Day award!

I’m keeping my eye on you at FinCon!

Also, are you bringing your wife?

Bring my wife? With you there?

Are you nuts??

jlcollinsnh recently posted…Mr. Market’s Wild Ride

I will be there. Did I mention that I’m bringing my pet Komodo dragon too? His name is Fluffy, but don’t let the name fool you. He is all business and all teeth. If you want to stay on his good side, you best bring some good beer to that party.

I’ll have some Bud Lite just for you.

BTW will, ah, Mrs. 1500 happen to be there?

In the comments on another site she called me “brilliant” while recommending my Stock Series and I, you know, just, ah, wanted to thank her in person. And completely…

jlcollinsnh recently posted…Mr. Market’s Wild Ride

Fluffy’s stomach is growling. Fluffy doesn’t care about the Stock Series. Fluffy can run faster than you and Fluffy is hungry.

Just found your blog from your link to my site… and I love your writing style. I’ll be keeping this on my blogroll, and will be checking back.

I never get tired of people trying to nitpick the 4% rule. Like you figured out, there’s so many ways to be flexible in your plan, which greatly increases the odds of success.

Hey Bo_knows-

Thanks kindly!

I have no idea why I didn’t have you on my own blogroll, but I just corrected that. Thanks for such an awesome tool; I could play with it for hours. Wait, that didn’t sound right. You know what I mean. I hope.

I *do* play with it for hours 😉

Oh me too! I even showed my wife your tool today, but she wasn’t even half as enthusiastic as I am about it…

An image none of us wanted…

This is an excellent post pointing out the humor to the “sky is falling” news stories the last two weeks. I will keep my eyes open for dinosaurs and Komodo Dragons. The good news is my wife has me house broken so the toilet seat and toilet paper concerns are not an issue!

I am using the 3% rule as my bottom line conservative number for planning. That said, I am not actually relying on my stock and bonds for my upcoming early retirement. That will certainly be the icing on the cake. Our plan is to be able to live on just our real estate passive income. Probably way to conservative for the younger FIRE crowd, but crap does happen and I plan to have a war chest of funds!

Bryan @ Just One More Year recently posted…4 Significant Lifestyle Changes in the Past 40 Years

Real estate is a fine way to go and I’m a bit jealous! I hope to follow in your footsteps and pick up a rental or two, but chances are slim as our market is nuts and I’m unwilling to go outside my area.

KISS reunion in your backyard? You should be so lucky!

Ha ha! I have a small yard. It would have to be Mini Kiss: https://en.wikipedia.org/wiki/Mini_Kiss

Wasn’t there also this article “China’s economy is doomed now – only because you lived by the 4% rule” (somehow “misplaced” the link as well).

As always a great rant.

I ran 3% calculations on FIRECalc and live by it. (So maybe India is also doomed only because of me.)

I saw an about 6ft long monitor lizard on a trip to Singapore once. It was amazing to witness such a fine animal with your own eyes. It is still one of my favourite memories of this trip. They are quite shy of people. So no danger for anybody.

Wow, didn’t know those things got to 6′, super cool!

I think I saw that article about China too. It was right after the one about the 4% meteor strike/tsunami catastrophe. Did you read about Tropical Storm Erika coming for Florida? It’s a little known fact that storms have middle names. Erika’s middle name is Four Percent.

Same here…I’d rather choose to be free than chained to my desk. But like you said in one of your comments, the math is easy…emotions not so much. There’s a part of me doubting that I’ll pull the trigger on early retirement. Firstly, living in a high cost of living area (NYC) with no plans to leave (most of our family/friends are here) makes it difficult to get there. Housing is the most significant expense. Then there’s the desire to pay for college for the kid/future kids as well as other things. Also, one thing that should be a plus is that I will have a pension…but with early retirement there is a hefty penalty. Yea…that’s the greedy part of me that’s choosing being chained to the desk.

Anyways, if the Komodo dragon is anything like an alligator/croc…I’ve heard that if you run zig zag you stand a better chance of outrunning them. It might be a myth so don’t take my word for it!

Andrew@LivingRichCheaply recently posted…Life, Liberty and the Pursuit of Financial Freedom

Friends and family are everything! I’d never leave NYC either if I were in your situation.

All of our family had already moved away from us, so we picked out a cheap place and moved there. Our 4 bed/3 bath place sets us back $1100/month (mortgage [3.25% @ 15 years], taxes and insurance), so we have an advantage.

Wow! If I had that much leftover I’d be retiring sooner rather than later!

Chris @ Flipping A Dollar recently posted…Ask the Readers: What’s your irrational fear?

Great post. A lot of people forget that the 4% rule also includes yearly raises (based on inflation rate), so that 40k per year in your example increases each year.

Steve Miller recently posted…App Review: Road Bike by Runtastic

I know, right? With that in mind, if you can just stick to the 4% for a couple years and forgo the raises, you’re setting yourself up for even more success.

This post was awesome, I certainly had a nice chuckle of the plastic dino eating the lego man! As far as the komodo goes I think my big red roo could take him http://i.imgur.com/DrUGB9i.jpg

Your comment about nitpicking that maybe “the world will continue to progress, but perhaps not at the same blistering pace”, I disagree with. I think as the world population continues to grow that economies will also continue grow. Just food for thought. Really enjoying the blog!

I hope you’re right about the future of the world! This is something I’d LOVE to be wrong about! Check in with me in 40 years!

Whoah, what is the story behind the kangaroo? I had a nightmare last night after I looked at that picture. Just kidding. Maybe.

My husband and I are debt free, own a home valued at $250K, rental homes valued at $350K and 401KS valued at $400K. If we retired today, in our early 40’s, we would only have our passive rental income because we cannot draw from our 401Ks until 59 1/2 years old. Would you recommend purchasing additional rental properties or putting money into the stockmarket above our contributions into our 401Ks?

Whoah, that is a tough question to answer without more detail. I’m going to muddy the waters further and propose something else. You don’t have to wait until you’re 59.5 to withdrawal from the 401k without penalty: Check this out: http://jlcollinsnh.com/2013/12/05/stocks-part-xx-early-retirement-withdrawal-strategies-and-roth-conversion-ladders-from-a-mad-fientist/

And this: http://www.investopedia.com/terms/s/sepp.asp

My viewpoint is if the 4% rule is a solid guideline, then shooting for a 3 – 3.5% withdraw rate will greatly improve your chances of success. And just because could withdraw 4% doesnt mean you will need to or should every year either. If the markets were to take a dive, I would certainly cut back on some spending also. Another consideration would be part time work. This could be something relatively easy and fun that brings in a few thousand a year. Examples like coaching sports, seasonal work at Home Depot/ Lowes, or if you are an accountant just working during tax season. Im sure many people have friends/ relatives that would hire them just to help out and many of these jobs have some good side perks as well. Plus I’ve found that if im working, then Im not out spending money! I actually dont mind working, its just that I dont care to have to be somewhere 5 days a week for 40+ hours! Plus like you mentioned, most people will eventually get some social security which will be some added income down the road.

* Sorry Mr. 1500, Jeff Spicoli already has Van Halen booked for his party 😉

“Examples like coaching sports, seasonal work at Home Depot/ Lowes, or if you are an accountant just working during tax season.”

I love the gig economy that we live in. Rent a room in your home (AirBnB), drive for Uber or Lyft or exploit some other talent you have on the Internet.

I think the key is frugality. If you can like on $40,000/year, making just $5,000 brings the 4% Rule down to 3.5% which makes a huge difference early on.

No Van Halen? Crap!

Came here from J Collins blog, This is a nice supplement to what he said in his blogpost. thanks

I didn’t know about the 4% rule. Thanks for sharing this informative piece. Educated me a lot.