Eight years ago, Dividend Growth Investor (DGI) asked me if I’d like to participate in the Warren Buffett bet. For those unfamiliar, in 2008 Buffett famously challenged the hedge fund industry:

Can you beat the S&P 500 over a period of 10 years?

Buffett won as the hedge fund got clobbered by the S&P 500.

But I like fun experiments and a little drama, so I agreed. Here is how it’s going.

Warren Buffett Bet: Year 8

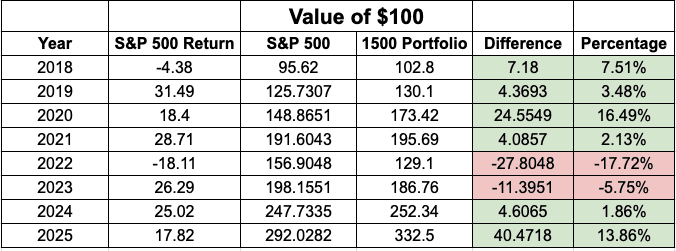

2025 was great! I extended my lead over the S&P 500 by quite a bit:

A 13.8% beat is pretty great! My compound annual growth rate is 16.2%. I’ll take that all day (and life) long.

But there are only 4 stocks in my Warren Buffett Bet Portfolio and they’re quite volatile. If any one of them take a big hit in the next 2 years, I’ll be in trouble.

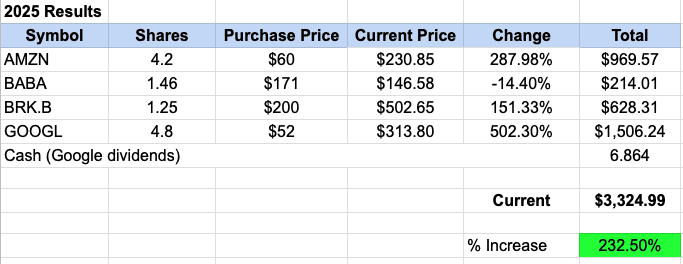

How My Picks Did In 2025

At the start of this experiment, I decided to pick four stocks (equally weighted) and not change anything for the duration. Here is their performance:

During this time period, the S&P 500 is up 192%. So half of my stocks are winning with Google crushing it.

Google, No Surprise (to me)

Google was down and out for a while because ChatGPT stole its thunder. But look now:

I’ve always liked Google for one simple reason; some of the most brilliant people in the world work there. I wouldn’t bet against Demis Hassabis and Jeff Dean.

Berkshire Hathaway?

I worry about the long-term prospects of this one. Berkshire’s top 3 businesses are insurance, trains (BNSF), and energy. All of these business could be disrupted by technology soon. Autonomous cars will be much safer than human driven ones, cutting margins for insurance companies. Autonomous trucking will supplant some of what trains so. Energy is changing fast, although maybe this will be a boon for Berkshire as demand surges.

Amazon

Amazon is a powerhouse in many ways. Everyone thinks of retail when they thing of Amazon, but its crown jewel is AWS.

Alibaba

This one was probably a mistake. I just don’t know enough about the company to assess it.

This Is What Was Supposed To Happen

Very few stocks outperform over the long haul. Most of the stocks in an index fund will be losers. But some will perform so well, it makes the whole deal worth it. My little portfolio is showing this in action. Google is killing it and Amazon isn’t too shabby either. But Berkshire is underperforming and Alibaba has been a spectacular dud.

Where Do We Go From Here?

I have no clue about my chances of winning this thing. I’m bullish on Google, but a lot can happen in two years, especially with a volatile tech stock. Disruption is happening faster than ever.

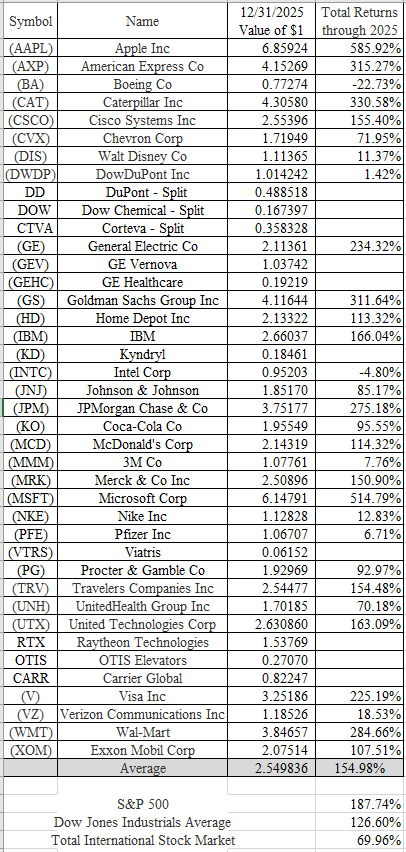

DGI’s chances of winning aren’t looking as good. This is from his update:

So his performance (154.98%) is behind the S&P 500 (187.74%). DGI has been fighting a difficult fight though. A dividend growth portfolio struggles to keep up when Mr. Market is in high growth mode which is exactly what has happened during most of this experiment. If the past 8 years had been flat or negative, DGI would probably be doing better.

I’ll be curious to hear his take at the end of the bet should he come up short. Does he switch to VTI? Unlikely. Does he stay with dividend growth investing. Most likely.

To be clear, I DO NOT wish to get into a holy war over investing styles. My goal as a growth investor is different from those who invest in dividends. I want to create the biggest nest egg while the dividend crowd enjoys regular cash flow.

My style is not for everyone. The price I pay for high growth is volatility that would keep many awake. Your money should not keep you awake and if dividends help you sleep at night, go for it.

In another example of prioritizing sleep over money, Morgan Housel likes to talk about how he paid off a 3.2% mortgage. He said it was one of the best things he ever did despite knowing that it was a horrible financial decision. I love cheap debt and will never pay my 2.85% mortgage off early. To each, their own.

To Index Or Not To Index

I like to play around with some of my money. When I notice something incredible and obvious (at least to me), I put money behind it. Here is one example:

SpaceX first landed a booster on December 21, 2015. The next company to successfully do this (Blue Origin), took almost 10 years. In those 10 years, SpaceX has landed over 500 boosters. Reuse means significant cost savings. When you perform a task for a lot cheaper than everyone else, one of two things happens. You:

- Expand the total addressable market (TAM) if you pass the savings on to customers. When a service or product becomes way cheaper, humans find new ways to use it.

- Keep costs the same and expand your margins.

SpaceX was a no-brainer investment to me.

But I’m also a big believer in index funds because they free up my mind to think about other things. I don’t want to be pondering the TAM of mass-to-space on a hike (yes, I’ve done this before). I have enjoyed playing the game, but all games run their course. I won’t be playing around much more, at least not with stocks. Instead, I’ll be on my skis, snowboard, or farting around with the keyboard or guitar.

Tune in next year for an update on 2027!

More 1500 Days!!!

You can also find me (and the dinosaurs) at:

- YouTube: My channel is mostly devoted to home improvement, but I have some other material coming up soon too.

- Instagram: Pretty pictures of dinosaurs, sunsets, and nail guns!

- Twitter: Spontaneous, often insane, ramblings

- Coworking space: On the surface, MMM HQ is a coworking space. Look a little deeper and you’ll see that we’re really building community. The members of MMM HQ are some of the finest people I know

- Buying a Tesla? Use my referral code to get some perks!

Your returns still amaze me. You winning the Warren Buffett bet, even while his own BRK.B shares are losing against the S&p 500.

Keep enjoying the good life, your numbers are so close to that 8 digit milestone! Just need another year like the last one.

Life is good!

Poor DGI. The guy should read the clear academic literature that indicates that dividends are completely irrelevant for investor returns. It’s not magic money being pulled out of nowhere. And to the extent that such stocks have outperformed in the past, that outperformance has been related to factors OTHER than the dividends. The dividends are an irrelevant sideshow. Ben Felix has some great content on YouTube about this.

I’ve never liked them either and don’t understand the appeal. If a company can’t think of anything to spend its money on, I’d rather have them execute a buyback.

I agree.

However, don’t say that to a dividend investor, they always talk about how “cash flow is king” and that dividend investing is so much better. Things like not having to sell shares to fund retirement, or deal with timing the market for when to sell. Never drawing down your number of shares…..

As they say personal financial is personal and if it helps them sleep at night to each their own.

I’ve been tracking my portfolio since the end of 2017. It’s a mix of ETFs and some satellite stocks. I found a calculator that calculated annual % return for the S&P 500 and it returned 14.34% in that time. My return was only 14.03%. I was weighed down by around 25% international and 10% bonds. In those ways, I was more diversified, but I also had the satellite stocks including Google.

It’s funny that it has come so close to just being a wash. My VTI was rarely above 20% and it has been around 6% since COVID.

Yeah, for me it’s almost a wash too. The longer I do this, the more I think I should just be in VTI and not pay it another thought,

Carl, you can do it!!! (Please imagine that I shouted this in the appropriate Rob Schneider accent/intonation).

I find your experiment highlights a key reality I see with clients all the time: concentration can accelerate wealth, but it also amplifies sequence risk, especially when only four holdings drive the outcome. From a tax perspective, low turnover and long holding periods—like you’ve done—are often underrated contributors to after-tax CAGR, particularly versus more active strategies. One practical consideration is harvesting losses strategically (as with Alibaba) to offset future gains while maintaining market exposure through similar assets.