My main goal* was to build an investment and cash portfolio of $1,120,000* ($1,000,000 to retire on and $120,000 to pay off the house) in 1500 days**, starting from 1/1/2013 and ending in February of 2017. I made my goal in 2016, my 1500 Days are over, and I’ve left my job. In the interest of openness, I’ll continue to share my numbers. For now…

I’ve Been Everywhere, I’ve Been Everywhere

One of the glorious part of not having a job is that as long as you can pay for it, you’re free to move about the world on your schedule.

In September, I took full advantage of my time and geographical freedom to partake in some adventures. First, I went to see my good friend Bob in New Jersey.

Next, Bob and I flew to Stuttgart to attend Cannstatter Volksfest with friends:

Then I moved on to Cancun for BPCon:

And finally, Los Angeles for the Tesla Robot day:

I’m in Atlanta now for FinCon and then Los Angeles in November for a college visit. After that, we’re sticking around Longmont. Travel is fun, but it’s also tiring and tedious after a while. My favorite way to experience life it to travel occasionally to experience new environments, people, and challenges. However, I want to live in a place I really appreciate and enjoy; that I look forward to returning to. This year, I went overboard on the travel part.

September

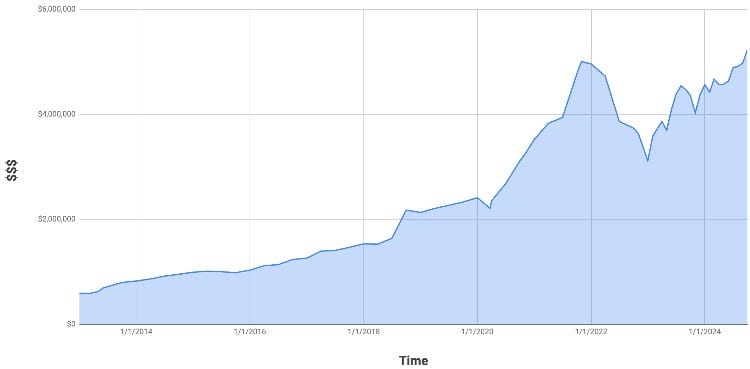

Our investments (not including primary home) started the month at $4,978,611 and ended at $5,230,934 for a gain of $252,322. We’ve never made anything close to 252k in a year, much less one month.

Never forget that your money can work much harder than you ever can.

All Time High!

If you’re an index stock market investor, you can expect returns of almost 10% per year (with dividend reinvestment) over the long term. That’s a stellar return. However, the price you pay for healthy returns is inconsistency. Some years are great. Others, not so much.

Our portfolio is now at an all-time high. The last all-time high was 3 years ago, way back in 2021:

What happened in 2021? Tesla stock was taking over the portfolio with an all-time high share price of $410. Back then, I probably convinced myself that the lofty valuation was justified. It wasn’t. The hype died down and the stock retreated back to reality. Mostly. It still has a speculative valuation.

Tesla note: If Tesla solves autonomy soon, its stock is undervalued. If not, it’s overvalued. I have no idea whether Tesla will solve it, but I remain skeptical.

Our money is in a curious place right now. Mindy makes money, but we’re also drawing down our portfolio. Just not that much. I like Wife-FI.

At this point though, we’ve passed escape velocity. We spend less than $100,000 year. As long as we keep living this way, our money should grow far faster than we can spend it. A 4% return on $5,000,000 is $200,000 per year.

Life is great!

More 1500 Days!!!

You can also find me (and the dinosaurs) at:

Mile High FI podcast:

MindyOnMoney podcast!

Also here:

- Facebook: Facebook group and page

- YouTube: My channel is mostly devoted to home improvement, but I have some other material coming up soon too.

- Instagram: Pretty pictures of dinosaurs, sunsets, and nail guns!

- Twitter: Spontaneous, often insane, ramblings

- Coworking space: On the surface, MMM HQ is a coworking space. Look a little deeper and you’ll see that we’re really building community. The members of MMM HQ are some of the finest people I know.

- Buying a Tesla? Use my referral code to get some perks!

*My goal wasn’t to have $1,120,000 at the end of 1500 days, but at any time before the day count was up. Why? It all goes back to the 4% Rule. Remember that our little friend, Mr. 4%, is nothing more than the most conservative safe withdrawal rate. Since my investment portfolio now sits at $1,550,000, I can spend about $62,000 in my first year of retirement.

**My original goal was $1,000,000 and no debt, I later raised the goal by $120,000 to $1,120,000 because I will have debt in the form of a mortgage and I firmly believe in not paying it off (LOOK at the MONEY I’m MAKING!). My compromise was to have enough money put away to cover the mortgage at the time of retirement.

***This is an affiliate link. If you sign up, the blog (me) makes some cold, hard, beautiful, cash. Personal Capital is a totally free and awesome way to keep watch over your investments. It’s worth it for the fee analyzer alone. I would never recommend anything that I don’t personally use and completely believe in, so give it a try. If you’ve already signed up through the link, please know that you are a fine person of above-average intelligence.

“…we’re also drawing down our portfolio….” ???

Whether it is this year, last 5 years or 10 years, you don’t seem to be drawing down your portfolio. Are you inventing a problem or am I missing something?

Again, congratulations on making the change from big saver focus to relax, spend and enjoy. Once you have enough, you should not worry how much your portfolio goes up each year. Yes, you do want to keep an eye on things when you invest in individual companies. But best to do what you are now doing …

I’m glad you made the shift! And I am glad you seem to be enjoying your new life.

I could have phrased this clearer. We are taking money out of our portfolio (we have sold assets to fund out life). However, our portfolio has grown much faster than we can spend it.

And yes, life is good! Better than I ever thought it would be. Much better.

“Travel is fun, but it’s also tiring and tedious after a while.” Totally agree with this. This year for me was lots and lots of smallish trips all around the US (and one to Oh Canada!). All pleasure, none business. I’m incrrrrredibly grateful to be able to take all of those trips, each having been loads of fun. But, man oh man am I glad to be done with travel for the year. There’s no place like home. There’s no place like home. . . .

Ha! Sounds like we’re on the same page!

Hey,

Saw you mentioned college visits. Any upcoming posts about FIRE and paying for college?

Oh man, that’s an interesting one, We didn’t do any 529 plans, so if we can get loans at a reasonable rate, we’ll do that. After that, it’s on us and my kid. We’re still trying to figure it all out.

We have family members who have been successful getting scholarships. There is supposed to be a lot of money out there for grabs. So, we have our kid working on that too.

Nice!

There have been some interesting threads on Reddit about income optimization to get full Pell grants with the new Fafsa

https://www.reddit.com/r/Fire/comments/1czkp12/actual_fafsa_financial_aid_results_for_a_fired/

Thank you for this. I just took a look at them and bookmarked.

Higher-level education is a hard nut to crack. Our older kid is dead set on NOT going to school in Colorado which will double costs.

**sigh**

Why loans? It seems like you have enough surplus to fund college.

Congrats on a new high. With the markets hot run my investments are also at a new high. Still not retired but seeing the value of my Stache not sure why I am still in the rat race.

Don’t overstay it! Life is pretty great here on the other side!

I read your first article where you said you could live off of 24-30k/year. What are your current thoughts about that? Could you live like that still? Do you think the difference is lifestyle creep/ inflation/ unrealistic numbers? Idk if there’s a wrong answer. But for us saying we could live off of 30-40k I’m curious to see if we’re delusional

If we had paid off our home, living off 24-30k would probably be doable. We decided to keep our mortgage ($15,600/year), so we’d need around $40k according to my original thinking.

If we really tried, I think we could get by on that for core living expenses: food, utilities, and insurance. However, we also bought 2 new cars.

We did figure out our annual spending maybe 5 years ago and it was around $65,000. I think we did underestimate it. And now, I wouldn’t want to live off that either. Definitely lifestyle creep in there. It’s not objects, just fancy experiences. And helping people too.

Living the dream! Looks like you’re spending less than dividend yield for VTI alone, so maybe you’re effectively not drawing down your portfolio, just spending the income it generates?

I feel the same with wanting to be excited about where we live and looking forward to returning home. We’re still trying to find that place after being thrown out of the USA – we need to travel to find it! Where would you choose to settle if the US wasn’t an option?

Do you measure your stock performance vs the index? Seems like you enjoy picking and continue to do it but I suspect you would have similar performance and less work/stress with VGT, etc?

I haven’t kept track, just because it would be a huge pain to do. Our portfolio is diverse and fluid. For example, we’ve done a lot of private lending (12% return), so we’re selling holdings from our solo 401(k) to lend. Money is always coming and going, so it would be painful to keep track of. We also have multiple Roth IRAs, an HSA, a rollover IRA, a self-directed solo 401(k), and a post-tax account. The last one has most of our stocks, so here is a screen shot of that that I took this morning: https://www.1500days.com/wp-content/uploads/2024/11/Screenshot-2024-11-03-at-6.18.30 AM.png

I do agree that index funds like VGT and VTI are the way to go. We’re very slowly transitioning our money to them.

“Travel is fun, but it’s also tiring and tedious after a while.” Totally agree with this. This year for me was lots and lots of smallish trips all around the US (and one to Oh Canada!).

“Travel is fun, but it’s also tiring and tedious after a while.” Totally agree with this. This year for me was lots and lots of smallish trips all around the US (and one to Oh Canada!). All pleasure, none business. I’m incrrrrredibly grateful to be able to take all of those trips, each having been loads of fun. But, man oh man am I glad to be done with travel for the year. There’s no place like home. There’s no place like home. . . .

Visit also: mehndi design easy and beautiful