My main goal was to build an investment and cash portfolio of $1,120,000* in 1500 days**, starting from 1/1/2013 and ending in February of 2017. I made my goal last year, but I have a lot of fun with these financial updates, so I continue.

There are loads of great things about being financially independent (FI). I think I’m a better, more honest person. Consider the following:

- No worries about what anyone thinks of you: Feel free to let your co-worker know what you really think of his shitty PowerPoint. If Bossman decides to fire you, you can be like:

- Be yourself: Now that I’m FI, I find that my true personality comes through more often than ever. This is not necessarily a good thing:

- And I can be my true self right here on the blog too: After 4 years of blogging, I’m still not exactly sure why email lists are such a big deal. However, every blogger who knows what they’re doing (the opposite of me) states that collecting emails is important. So, I signed up for a fancy service to try to persuade you to give up yours. I can’t take it seriously, so I configured a couple of my forms like this:

Life is just a lot more fun when you don’t have to care. And it’s even more fun when you don’t care.

Performance Update

February was another great month. My portfolio went from $1,316,646 to $1,351,858 for a gain of $35,211. $1,47o of this gain was from 401(k) contributions.

When I add my portfolio to my home equity ($350,000), cars and other stuff ($20,000), my net worth comes out to $1,721,858. February was the first month I passed the 1.7 million mark. Life is good.

Can $2,000,000 be far off? Maybe. If I reach it, what do I call it? The Double Double Comma Club (DDCC)? That sounds clunky, but I don’t have have a better idea, so I’m sticking with it.

I have a better chance of joining the DDCC some day if one or more of the following happens:

- Mrs. 1500 stays at her job for a while longer: I put no pressure on her. She can do whatever she wants (she ignores me anyway).

- We pull off some real estate deals: I’m trying to work multiple deals including the home next to us. I’ve also been thinking about getting a piece of land in a mountain town near us and building a cabin or two.

- Physician on Fire (PoF) sends me $100,000: I was studying PoF’s Investor Policy Statement when I noticed an empty space at the bottom of the Other category. I immediately added my own line item:

Now I cross my fingers and hope that PoF, in a lapse of judgement clouded by laughing gas and beer, sends me the money. Or maybe not. PoF caught wind of my scheme and replied with this:

February Update

2017 (as of 2/28/2017)

- Days elapsed: 59

- 2017 gains: $94,710, (including 401(k) contributions of $11,470****)

Since the start (1/1/2013)

- Days elapsed: 1517

- Gains since 1/1/2013: $765,815

- Needed to quit work ($1,120,000 in investments): Mission accomplished!

- Net worth*****: $1,721,858

Exercise and the Beer-O-Meter

My P90x routines were P90meh. The fire just wasn’t there. I recently started mixing the routines up with kettle bells to break up the monotony. The good news is that my gut continues its downward trajectory, although my weight loss decelerated:

Not many changes in the body though:

I vowed last month to cut down on beer. It didn’t work out so well. My February consumption was identical to January. I’ll try harder in March.

Spending: $2,442

We’ve recently started tracking our spending. I’m not thrilled that we plowed through $2442.36 in February. The items that disturbed me most were Food (grocery store) and Food out (restaurants). The Beer category looks disturbing, but most of the spending was on birthday gifts:

This doesn’t include our mortgage/tax/insurance payment of $1246.49. We have enough cash to pay off the mortgage, but don’t because I like to leverage debt. If I add all of that up, it comes out to $3,688.85 for the month or about $44,000/year in spending. According to the 4% Rule, this would require me to save $1.1 million. I have $1.3 million, so I’m good. Besides, I only have 11 years to go on the mortgage.

My $10,000 Experiment

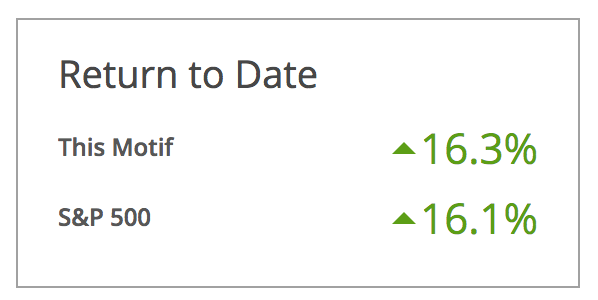

I started an experiment to convince myself not to pick stocks. I picked a basket of my favorite companies and threw $10,000 at it. The goal here is to lose to the S&P 500 so I no longer want to pick stocks. Unfortunately, I’m winning, so the experiment isn’t going well. Or maybe it is. I don’t know.

I started an experiment to convince myself not to pick stocks. I picked a basket of my favorite companies and threw $10,000 at it. The goal here is to lose to the S&P 500 so I no longer want to pick stocks. Unfortunately, I’m winning, so the experiment isn’t going well. Or maybe it is. I don’t know.

Finally, we moved another $100,000 out of the markets and into real estate. We funded a hard money loan to bring our real estate investments up to $245,000 (one other hard money loan of $95,000 and a private equity investment of $50,000). More on this when I write about my portfolio in a couple weeks.

*My goal isn’t to have $1,120,000 at the end of 1500 days, but at any time before the day count was up. Why? It all goes back to the 4% Rule. Remember that our little friend, Mr. 4%, is nothing more than the most conservative safe withdrawal rate. So, if I were to quit my job now, I could spend about $48,000 in my first year of retirement. I’d stick very close to that number too because market valuations are ambitious. Let’s say that Mr. Market caught a cold tomorrow and my portfolio dropped down to $800,000. No big deal. This would mean I’d be safer stretching my spending a little north of 4%.

**My original goal was $1,000,000 and no debt, I later raised the goal by $120,000 to $1,120,000 because I will have debt in the form of a mortgage and I firmly believe in not paying it off. My compromise is to have enough money put away to cover the mortgage at the time of retirement. So, to retire today, I would need about $1,120,000.

***This is an affiliate link. If you sign up, the blog (me) makes some cold, hard, beautiful, cash. Personal Capital is a totally free and awesome way to keep watch over your investments. It’s worth it for the fee analyzer alone. I would never recommend anything that I don’t personally use and completely believe in, so give it a try. If you’ve already signed up through the link, please know that you are a fine person of above-average intelligence.

****My 401(k) contributions include my own, Mrs. 15oo’s, and the contributions from my corporation. Self-employment with a solo 401(k) is a very powerful savings tool. I should have done this years ago.

*****The numbers on the right side of the page only reflect my investments and cash. Net worth includes, but is not limited to:

- Home equity ($350,000 after the appraisal!)

- Cars

- Bicycles

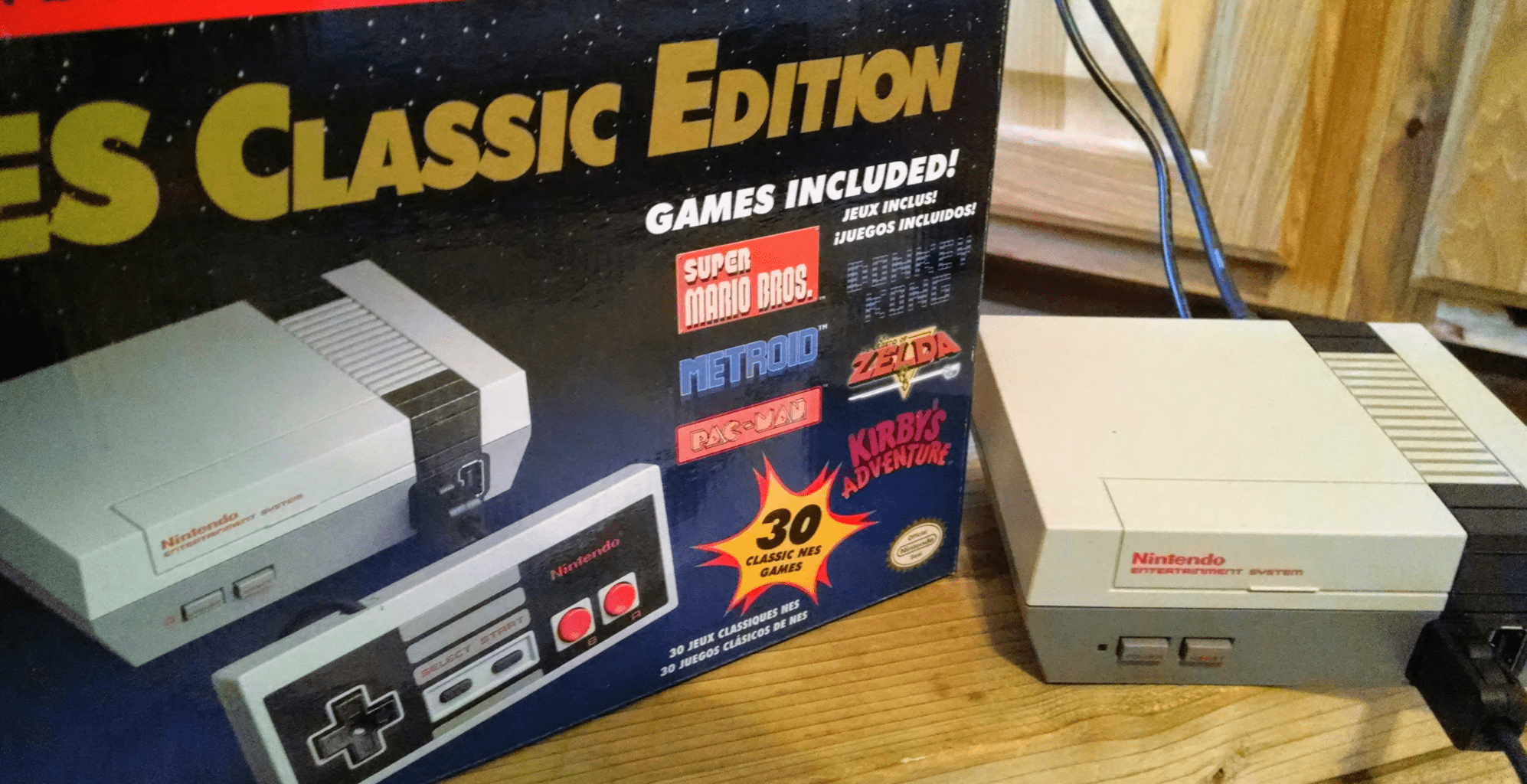

- NES!: When I was a kid, I saved up for months to buy the original Nintendo. And I loved it. Games like Metroid and the Legend of Zelda amused me for long periods of time. One of my goals once I fully retired was to play more video games (eagles may soar, but weasels don’t get sucked into jet engines). Last year, Nintendo announced that it was releasing many of the old games on a new system, the NES Classic Edition. Despite their great games, Nintendo is a shitty company that purposely keeps supplies low to generate hype. Four months after the initial release of the NES Classic Edition, they are still selling for triple the retail price on reseller sites. I was tenacious and managed to get one by standing in line at a Target for 15 minutes before the store opened. Life is good. And slightly less productive.

Haha… best email sign up forms EVER. You’ve gotta split test these now.

Nice momentum on your way to $2M! You’re about to blow right past me (unless I can convince PoF to give me your $100k).

Looking forward to hearing more about the 4-plex saga one day soon. Good luck, my friend. 🙂

Michael @ Financially Alert recently posted…My 40 Year Advantage is Now Yours

Thanks Michael! I may pass you, but you still win because you’re at least a couple years younger than me. By the time you hit my advanced age, you’ll be far past where I was at the same time!

You will get nothing and like it, Michael!

PhysicianOnFIRE recently posted…Successful Blogging: 10 Steps to Building and Growing a Website

You are killing it!!! Mrs. Bayalis said I had to share with you about my last day at work. I recently switched jobs and I had some weird co-workers. One left a message in my going away card that said “You taste like Jelly. Love, Dinosaur” Thought you’d get a kick out of that. Or maybe you’re secretly working and were my co-worker 🙂

Mustard Seed Money recently posted…The Journey Out West

Wow, that card is hilarious! And slightly disturbing. Maybe it’s a good thing that you’re no longer there!

I love those sign-ups! I would totally sign up for an e-mail contact list if it said that. After all, how can I ignore the wisdom of tens of people? 🙂

It reminded me of something I saw on Reddit personal finance a while back that my husband and I still use with each other. It was someone sarcastically mocking frugal people, by talking about how wealthy they were, splurging “threes of dollars” on a Big Mac. Sometimes we’ll use that when debating a small purchase – do we really want to spend “twos of dollars” on that thing? Lol.

Those 14 people who have signed up are pretty smart!

And a Big Mac is too rich for my taste. I usually go for the Happy Meal!

Haha, I wouldn’t be surprised if your email signup forms are effective.

Nice to see that portfolio growing. So far 2017 is off to a big start for all of us passive investors.

Biglaw Investor recently posted…Do You Need Disability Insurance?

Yeah, they have been more effective! Funny how that worked out.

And yeah, markets are flying. I think the party will end soon, but enjoy it while it lasts. Since I’m still in saving/investing mode, I wish the party would have ended a long time ago.

Very cool finding the nes. I tried several time before Christmas but the lines starting at three am discussed me. 15 mins before is much reduced. I suspect this time next year they’ll be on discount, in typical Nintendo fashion.

I HATE Nintendo. Why to they do this? The only ones that benefits are the jerk scalpers.

I think I’ve only ever signed up for two e-mail lists. One promised eternal life (so far, they’ve delivered) and the other is 1500 Days.

The Vigilante recently posted…Basic Training, Vol. 7: Why You Should Never Feel Investor’s Guilt

Ha ha, thanks Vigilante!

99% Fart Jokes!? Man, you must have a bunch of ’em….

The well runs deep. And stinky.

Haha. I love the email list messages. Great progress up towards $2 mil. You’ve had some pretty incredible growth over the past few years. Hope the stock market keeps chugging along!

I’m interested to see how your motif portfolio does against the S&P. Fun idea. Maybe you’ll find your hidden talent as a stock picker!

Go Finance Yourself! recently posted…Live a Longer Life With Purpose

Motif! Yeah, I actually have done very well as a stock picker. I bought Google in 2004, Apple in 2007 and Facebook in 2012. Because I still hold at least half of these shares, I’ve greatly outperformed the S&P 500. However, I don’t think I can do it over decades.

Dat progress tho. Looking good! (For both physical and portfolio changes lol)

Gwen @ Fiery Millennials recently posted…Fiery Millennials: Year Two

You’re too kind Gwen, but thanks!

Hahahaha! Honesty in email signup forms; I dig it. 🙂 PoF needs to hurry up and send over that $100,000. I mean, it’s in his policy statement, after all. Not sure if this helps with the beer problem, but Mr. Picky Pincher opts for higher quality beer to cut down on consumption. He gets more sippable beer instead of chuggable beer.

Mrs. Picky Pincher recently posted…What A Frugal Blogiversary!

“PoF needs to hurry up and send over that $100,000.”

I know, right? Come on PoF! Show me the money! Or not…

Gotta love wisdom from Caddyshack! Wow that’s a huge gain. Your portfolio, not anything body related. I once tried a 30-day no alcohol challenge and I didn’t see any difference. Maybe it’s because I substituted wine for chocolate? hmmm

Yep, no difference in body except for the 1 pound I lost. Oh well, I think March will be better…

So when the video games get glitchy can you still fix it by blowing on them like a harmonica? Also does it have duck hunt? Growing up in Montana, duck hunt was my jam.

Oh wow, I remember the blowing trick (yikes, that sound dirty)..

This is a fun update post. Nice going as always, and two quick things:

1) Yes, finally a Caddyshack reference! Although I fully appreciate both Airplane and Ferris Bueller memes, it’s nice to see another 80’s classic being represented.

2) How great is the NES Classic? I, too, was lucky to get one as well at a Target before it opened. Hope you’re enjoying it.

Oh man, I LOVE the NES Classic! I almost wish I never got it, too much wasted time…

I’m actually surprised you bought a retro NES giving your programming background. Little bit of work on a Raspberry Pi and you can have an NES with more than 30 games. Built a couple for family members one year for Christmas, need to get around to building one for myself for when my son is old enough to play.

Yeah, I heard about this. I’m extremely time constricted and the NES seemed like the path of least resistance. I would like to fart around with the Pi in retirement though…

Can I sign up to both the e-mail lists? I need more stuff in my in-box. Have you starting asking people to pull your finger yet?

Nintendo is evil. They made my son wait in line for his new switch system. Which BTW he saved and side hustled for.

Congrats on the great month!

Brian recently posted…Interview Series: A Journey We Love

A Switch! Whoah, cool! Nice work on his part hustling for it. And nice work on your part making him work for it!

I noticed your e-mail sign-up form last week. It gave me a good laugh. 🙂

Good job with your portfolio last month! You’re rocking it. Why are you still working again?

“Why are you still working again?”

Funny you mention it. I gave notice last Friday. You’re the first to know! 🙂

Congrats!!

Haha, funny post today Mr. 1500.

I don’t understand why email lists are important either…those sign-up pop ups everyone has sure are extremely annoying. At least your forms are pretty funny/honest.

Your February spending was impressively high at $2442. Is this a typical number for you? Am I also correct in remembering you guys still have a mortgage on top of that too?

Mr. Tako @ Mr. Tako Escapes recently posted…Rich People’s Driveways

Our spending was high. Mrs. 1500 has to get a better handle on our food purchases. She is a hoarder by nature and this extends to the refrigerator. We end up throwing lots of food in the garbage. Once I have fully relieved myself from my job, I’m going take over food for a while and get things whipped into shape. We also spend $225 on more ski lessons.

And yeah, we have a mortgage payment of $1246 on top of all of that. 11 more years to go.

I would be curious to hear more about your real estate deals.

The RE market here is pretty crazy as well – with bidding wars for properties that need significant work visible even to a neophyte like me.

Dividend Growth Investor recently posted…Colgate-Palmolive (CL) Dividend Stock Analysis for 2017

Real estate is the same way here, so we just fund other people now, always making at least 10%. In the case of the hard money, we’ve put money behind just one guy who we trust completely. We’re first in line on the lien though just in case something goes bad. I’ll write about it more when I post about my portfolio in a couple weeks.

Nice work!

That NES looks cool although SNES was more my era, you can get most of those games downloaded for peanuts on the Wii&Co so one day I’ll get around to pulling ours out of the cupboard and giving them another go.

I’d chill on the 2400 expenses, that’s pretty frugal by most people’s standards I’d say. good food and beer is the corner stone of a happy life 🙂

One thing, I can’t see any serious mortgage payment in there, is it really that small that it gets eaten up into “bills” or other?

Ha, nope, I don’t include it. Maybe I should though? I have mixed feelings because we have the cash to pay it off and it is a temporary expense (11 years to go). Oh screw it, I just updated the post.

I think the reason that you are failing to lay your hands on the 100k from PoF is

a. You lack an accomplice (<——– subtle hint) and

b. Your plot isn't anywhere near complicated enough. There needs to be at least one botched kidnapping, a high speed chase, a dinosaur, and many pairs of really dark sunglasses being worn by everyone involved.

Mrs. BITA recently posted…The Quirks of Being Middle Class Indian (and how it benefits my wallet)

Ha ha, it just so happens that I’ll be in PoF-land later in a couple months…

Awesome! You’ll be a multimillionaire soon.

I was hoping to play more video games when I retired too, but it just didn’t work out that way. There wasn’t anytime to play games with the kid around. Now that he’s a bit older, he is more interested in video games and we play a bit more. The missus doesn’t like it so we still have to put some limit on it.

The 4-plex will keep you busy for sure. The link to the 4-plex post doesn’t work, BTW.

Bah, I don’t know what happened to that post? Grrrr. Thanks for letting me know.

I just walked past the 4-plex yesterday. We’ve gone as far as talking to the owner (well over 90), but I don’t think I’ll ever buy it. It brings in around $8,000/month ($96,000/year), but I’m thinking I’d have to cough up $1,200,000 to get it. There are a lot of fools around who overpay…

RE 4-plex. Taken from a friend … Write up two purchase offers. One is lower than the purchase price by 15%. The second office has the same price plus the sweetener of your offer to pay his capital gains taxes (the market value). This transaction is about feelings not rational pragmatic thinking.

What does an 80 year want to own property for anyway?

Ha, she’s over 90. And she owns a couple of them.

It isn’t for sale, so we were trying to get it off market. Once it hits the market, we have no hope at all.

1500 days – Only blog in the world to combine Judge Smails, physical fitness, financial education and retro video games in a single post. SO MUCH CONTENT! Where to begin…perhaps you should start tracking the relationship of your beer spending to your blog creativity – there is a high correlation recently as you have been killing it!

Am very intrigued with your private equity investment – can’t wait to hear about the project and the decisions leading up to it.

February was a good performance month, but personally was happy to complete the consolidation of all of our retirement savings from various places into a single Vanguard account. You would be surprised how long certain brokerage houses take to transfer an account.

Good luck with the Triforce of Power.

“It’s easy to grin when your ship comes in and you’ve got that stack market beat. But the man worthwhile, is the man that can smile when his shorts are too tight in the seat.”

Hey Jeff!

Thanks for the kind comments!

Private equity is with a real estate syndicator called Praxis: https://praxcap.com/ They have a stellar reputation, but you must be accredited and the minimums are usually $100,000.

“February was a good performance month, but personally was happy to complete the consolidation of all of our retirement savings from various places into a single Vanguard account.”

You’ve achieved singularity! Nice! I still have at least 8 different investment accounts. It drives me nuts. Some day, I’ll be like you…

I beat Gannon last week! Much easier now with the online walkthroughs! 🙂

Nice poem Robert Frost!

Putting a humerous context around FIRE… I will await the fart sign up email list before taking action!

The biggest beneift is that you can always be yourself, no matter what. When people do not like it, so what?!?

“The biggest beneift is that you can always be yourself, no matter what. When people do not like it, so what?!?”

I know, right? This is a personality defect/weakness that I have. I’m more confident with a big nest egg which is completely silly because it’s stealth. Go figure. At least I’m honest about my craziness!

Hey I’d say your Food and Food Out spending is pretty good! We spent $2k last month on food. I’m not exactly sure but I think we may have accidentally eaten some of our money. It looked like lettuce. Leafy greens. And so on.

I’m new here — what’s the beer of choice? Something frugal or something crafty? –R

Rich @ pennyandrich.com recently posted…Rich’s Plan To Build A Generational Family Legacy. Uh, Yeah, In 3 Easy Steps!

Whoah, $2,000! Are you eating at Brazilian steakhouses weekly? 🙂

Beer: Just like every other person, I like the hoppy IPAs. Pliny the Elder and Heady Topper are two stellar examples.

So in your monthly budget, where’s the health insurance? Is that the tiny $228.93 med category? If so, I would love to find out more about how you achieve that low figure.

Hi John-

My wife is fortunate enough to get it through her job (neither of us are fully retired yet). I’m leaving soon though and she stays on because she loves her work.

In any case, when she does leave, we’ll go through an organization like Liberty HealthShare which will set us back about $500/month. Here is a great review of the company: http://clubthrifty.com/liberty-healthshare-review/

Cool…kinda thought that was it. I’ve been “retired” for some years, and am just over 50. My wife has a chronic condition so liberty is not a consideration. Our insurance through the exchange is (would be) about $1800 monthly, and her OOP expenses totalled around $25,000 last year. We cut out my “play work” so that income is well under poverty level so we can get the subsidy. It definitely adds pressure to the overall picture, but thanks to the market last year and rental incomes, our net worth actually went up a bit. Not too hopeful to keep that condition though.

Thanks

I feel for you and I’m sorry to hear about your wife’s health issues. I’m so thankful that my family has been healthy. A chronic health condition would certainly change everything.

I think you are entitled to having one spendy pants month, which isn’t even really that much of a spendy pants. And the best part of the post…the Caddyshack reference. I will be drinking a beer in your honor as I watch it tonight while we have snowpacalypse in New England.

My P90x returns are starting to diminish as well. Probably due to a reintroduction of carbs and beer.

One thing I’m not going to miss about work is the endless amount of PowerPoint slide decks. Putting the same amount of words from a document on a slide doesn’t make it a presentation!

I’m also interested in learning more about your real estate investments. Would the cabin project be a new build?

Mr. Need2save recently posted…A Different Kind of March Madness

I decided last night to take a break from P90x and focus on weight loss. I just don’t have the motivation to do P90x at the moment. I’ll supplement the running with kettle bells and push-ups.

Real estate! I’d love to do a new build with modern design and construction (structural insulated panels). Good land is hard to come by, so maybe we’ll buy something old and rehab it. I’m open to anything right now.

So jealous you get the NES Classic. I’ve given up trying for the time being. It needs to come back down to the $60 price point.

Great job reaching your financial goals! Its inspirational to see someone set similar goals to me and reach them as planned.

Sorry about your NES failures. Don’t give up; it’s worth it!

I recently read a post on Ultra Running that also featured dinosaurs. You get around don’t you.

Great update. Your posts are almost always entertaining. I must ask though, why are you blaming our wife for the food overages? Do you not do any of the cooking? And what you spent on beer? Yikes. I’m glad I don’t drink. Looks like that alone saves me a ton of $.

She buys the food and does all the cooking. She doesn’t do it efficiently though (“I hate leftovers!”). And she buys too much. Our freezers (yes, we have multiple) are so packed, I don’t even open the doors because of the avalanche of stuff that falls out. The solution to this is for me to take over the food which I’ll do after I retire.

As I said in the post, the alcohol cost was mostly due to expensive bottles of liquor we purchased for gifts.

New to your blog. From what I gathered from your blog, your wife is still working, so currently you do not need to withdraw from your joint retirement accounts… which enable them to continue to grow, correct? Do you consider yourself as an individual FI… or as a couple are you FI? For discussion, let’s say your wife, like you, did decide to retire. Your goal was $1.12M which at 4%, as you said, would generate about $44K or about $3.7K per month. While 4% is widely considered a relatively safe rate for a 30 year retirement, at 43 with 45+ years of retirement to plan for, I’d think you’d be safer at 3.5% or 3.0%. COL adjustments really take their toll in the latter half of your retirement, which is why 4% is really only advised for 30 years. Maybe I’m missing something, but at a safer 3% withdrawal rate and assuming with your wife retiring that you need to factor in health coverage along with your mortgage for 11 more years… you’re not gonna make it on $1.12M or even the $1.35M you’re currently at. 3% of $1.35M is $40.5K BEFORE Tax. Even assuming ½ of this is tax free (Roth IRAs?) and the other ½ is taxed at 20%… it’ll leave your NET right around $36K or $3K per month. Minus your $500 per month estimate on health coverage (which is optimistic given the uncertainty right now)… you need to be living consistently now on an average NET of $2,500 per month including your monthly mortgage payment and averaging in all other cyclical expenses like taxes, insurance, appliances, home repairs, automobile repairs, other rainy day stuff, etc. Curios to know your thoughts? Did I miss something? Best of luck to you and all who endeavor to FIRE.

Yep, the wife is still working! And I am too, but only part-time and not much longer. I am comfortable with her quitting at any time though. She loves her job, so she’ll probably hang on for a bit longer which I fully admit is a boost to our chances of success.

I think we have a difference of opinion here: “I’d think you’d be safer at 3.5% or 3.0%.” 4% is the floor. In most times, your could go higher. Have you read Kitces article: https://www.kitces.com/blog/the-ratcheting-safe-withdrawal-rate-a-more-dominant-version-of-the-4-rule/

I’m sticking with the 4% which would give me $52,000 per year in spending per year or $4300 per month (bases on 1.3 million). Now, $4300 is pretty close to our spending in retirement ($2500 + $1250 (mortgage) + $500 (health insurance)). However, the mortgage will go away in 11 years. Also, we have real estate investments which return 10% or more. Of course, there is risk there too, but nothing is completely safe.

When we both quit, we’ll be very conservative initially. If things go bad (stock market drop of 50%) in the first 10 years, one of us will just go back to work. Flexibility and frugality is the key.

At this time, I also acknowledge that the blog makes money too. Not much, but little bits go a long way when you live a frugal life. The 4% Rule assumes no future income, not even social security. I enjoy making money and social security is a sacred cow that no politician would kill. Hell, our stupid politicians are even too scared to take logical steps like delaying the age in which folks can receive benefits.

Finally, I understand your concerns. I’d be lying if I said that I didn’t think about this same stuff every damn day. I don’t like how expensive markets are now. I also don’t like the uncertainty that our new president brings to the table. However, there is risk on both sides of the FI equation. I consider staying at my job too long a risk as well. You only live once after all.

Also, at least $500,000 of our portfolio is after tax. Since our income will be low in retirement, these will be completely tax free: http://www.bankrate.com/finance/taxes/no-capital-gains-due-for-some-investors-1.aspx

Oh, I should also mention that on top of the 1.3 million portfolio, we have $350,000 in home equity. I keep it separate because that money isn’t working for me. However, that money isn’t useless either. Someday, I’ll probably sell the home and move to a cheaper area or rent.

Thanks for your reply. Good read on the 4% rule. Knew based on Monte Carlo simulations that it was playing it quite conservative, but never saw the 2/3 or 1/2 of the time figures showing just how safe it was. And I was missing something in your story… besides your magic number for your retirement assets, I hadn’t factored in your other sources of income… rentals, blog, etc. Looks like you’re in pretty good shape. Again, very much appreciate your wiliness to share a reply and make me think. We’re 46/47 now. With 3 kids to get through college, we’re shooting for FIRE at 52/53. I share your optimism about Social Security… too big to go away completely… so hopefully just a nice little bonus. And if for some crazy bad luck we retire under the worst market timing ever, if the 4% rule turned out to be too aggressive between 52 and 62, some level of social security should help us adjust and give our retirement accounts time to recover to healthier levels. And then there’s always inheritance. Can’t count on it… but odds are decent enough there’ll be something coming our way. I don’t do risk well. I’m playing it very safe. It’s likely I’ll be one of those retirees 30 year later that way over-estimated what we needed. I’ll be O.K. with that as long as I’m still alive to enjoy it.

Can’t wait to see you hit the $2 mil mark, be interesting to see what your thoughts are when you hit is and then again when we have our first market correction in about a decade. Thanks for the inspirational posts!

Ha ha, I may never hit it! Markets are expensive and could use some downward movement…

So I get you want to get in shape, but what’s wrong with 0.6 beers per day, nothing at all, I bet money you can find a study that says beer is good and consumption of beer is healthy, like many things in moderation.

Our food budget is one our bigger expenses, but it’s also one of the things we value most, regardless of eating in or eating out we spend a few dollars more, I could blame it on my dog since I include all of this into the “food budget” but I’d like to keep my dog on the good side of finances.

I also like this new found aggression towards real estate, is the Mrs. promoting this by any chance? I think she is;)

Steven recently posted…Simple is Always Better

I love your sense of humor. The sign up forms are fantastic!

On a side note I noticed that you said you started tracking your spending. I haven’t been following the blog too long but if you haven’t been tracking spending, then how do you know what you need for a 4% SWR?

Hey AJ!

I’m glad you like my forms!

We had a basic idea of our spending, having done it before. As retirement nears, I wanted to know for sure.

Fart jokes! Almost enough to convince me to sign up for your email list…

With Respect to the what-comes-after-Double-Comma-Club issue, it goes like this:

One1111111One! Club (More than $1,111,111)

Fibonacci Club (More than $1,123,581.321)

One-Two-Three-Four-Five-Six-Seven Club (More than $1,234,567)

Four-Thirds Club (More than $1,333,333.33)

Golden Million Ratio Club (More than $1,618,033.9887)

Double Dime Douchebag Club (More than $2,000,000)

e Club (More than $2,718,281.828

Pi Club (More than $3,141,592.65)

After that I guess it’s open road till the Triple Comma Club.

Math major?

This is totally awesome! And I never thought I’d say this, but I really want to be a Douchebag someday. What, I already am?

Now that I am FI I definitely feel free to give my honest opinion at work. Heck it may even increase my odds of getting laid off with a hefty severance package!

I see you are looking at getting some land and building some cabins. Also heard Mad Fientist mention it in his podcast. Are you going to write about that soon? I’ve been looking into doing the same thing in Colorado.

“Heck it may even increase my odds of getting laid off with a hefty severance package!”

That is awesome and congratulations on your FI-ness!

“I see you are looking at getting some land and building some cabins. Also heard Mad Fientist mention it in his podcast.”

Yes! The Mad Fientist and I may even be plotting something together… Where in Colorado are you looking? Let’s buy a big chunk of land, subdivide and build FI-town. In the middle of FI-town will be a water tower with a smiley face, rainbow and raised middle finger. Do you want in?

And yeah, I think this would be fun to write about. Stay tuned…

“Do you want in?” – Actually this sounds pretty awesome…

I’m still in the early stages and casting a wide net. Something with year round access and convenient to skiing but not too close to the mega-resorts. I’m new to the Colorado real estate scene and will definitely be following along.

I think you are entitled to having one spendy pants month, which isn’t even really that much of a spendy pants. And the best part of the post…the Caddyshack reference. I will be drinking a beer in your honor as I watch it tonight while we have snowpacalypse in New England.

FI is the definition to me! I’m a worker. I have to work more than 8 hours per day. I see your success following your writting but how can I choose the true jobs for having FI as same as you? Amazing with your FI. Thanks for sharing!